Jump to the section that meets your immediate needs best:

Average Cleaning Business Insurance Cost (2026 Report)

Average cleaning business insurance costs range from $293 for a starter bundle to $559 per month for a more comprehensive policy set.

However, your costs will depend on the type of cleaner you are, where you operate, the coverage types you need and how large your company is.

If you are ready to get quotes, we can match you with the cleaning business insurer that fits your needs below.

Select state

Updated: July 24, 2026

Advertising & Editorial Disclosure

How Much Does Cleaning Business Insurance Cost?

Cleaning business insurance costs for a starter bundle average $293/mo, according to my research. This starting bundle includes coverage that meets the most common requirements for cleaners and protects you against common risks, such as client slip-and-falls, third-party property damage, employee theft and vehicle accidents when driving to and from job sites.

However, this only represents the minimum viable policy set. As you add employees, lease property for your company's equipment, and get commercial clients, you'll take on more financial risk and additional requirements. In light of this, I've broken down the bundles that apply to most cleaning companies, what they include, their costs and who they apply to.

Starter bundle | General liability, commercial auto, janitorial bond | $293 | Startup cleaners and sole proprietors |

Standard bundle | Starter bundle + tools and equipment | $331 | Solo cleaners with equipment and tools over $1,000 |

Growing Bundle | Recommended bundle + workers' comp | $466 | Cleaning companies hiring their first employee |

Established business bundle | Growing bundle + commercial property and umbrella liability | $559 | Cleaners expanding to commercial clients and leasing a building |

While this table represents a general cleaning company, it is not specific to your profession. For example, a maid service would pay $271/mo for a starter bundle, which sits below the generalized average. Explore more specific costs for your profession below.

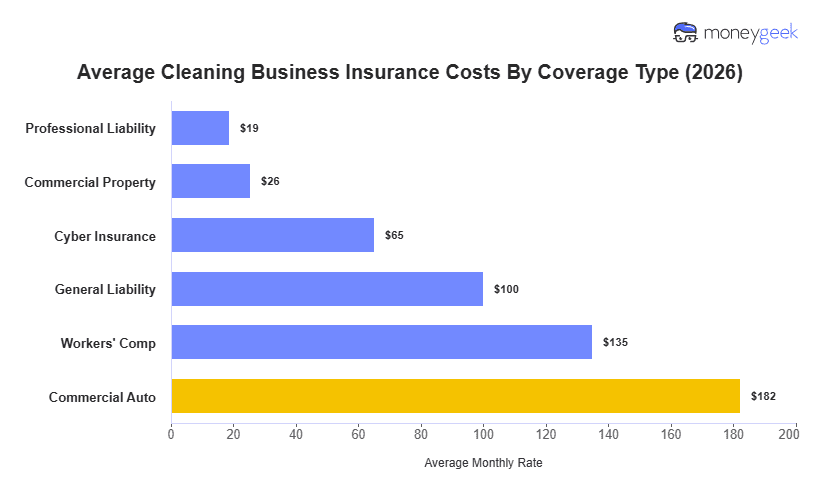

Cleaning Business Insurance Costs By Coverage Type

In short, cleaning insurance costs for common coverage types are as follows:

- General liability: $100/mo

- Commercial auto: $182/mo per vehicle

- Janitorial bond: $11/mo

- Tools and equipment: $23/mo

- Workers' comp: $135/mo per employee

- Commercial property: $26/mo

- Commercial Umbrella: $65/mo

- Professional liability: $19/mo

- Pollution liability: $223/mo

- Cyber Insurance: $65/mo

An average cleaning business's insurance bundle often includes many of these coverage types, each with its own inclusions, requirements and costs that vary depending on your company's risk profile. Not every one of these will be necessary for your business, but it is best to understand each so you only buy the policies you need. The dropdowns I've provided below give this context.

Cleaning Business Insurance Cost Estimate Calculator

Enter your business details, and the coverage types you want to get insurance cost estimates tailored to your cleaning operation. If you'd like, this business insurance calculator also allows you to be matched to an ideal provider in our network based on what you enter by clicking Get Quotes.

Before using the tool, keep these items in mind:

- No personal details are gathered or stored, and you will receive no spam

- Workers' comp estimates are calculated on a per-employee basis

- You need to enter your particular type of vehicle for commercial auto costs

Estimate Cleaning Business Insurance Costs

Select your state and industry to view average business insurance premiums in your area. Rates are calculated based on a business with 5 employees and $500,000 in annual revenue.

Select Coverage Type

Select State

Select Employee Count

Select Vehicle Type

Monthly Rate Estimate—

Select Coverage Type

Monthly Rate Estimate—

Select State

Select Employee Count

Select Vehicle Type

Factors Affecting Cleaning Business Insurance Costs

Several factors shape cleaning business insurance costs, and two operations with identical coverage can pay very different premiums based on where they operate and how they run. These are general cost drivers, and how much each one affects your premium depends on your specific business profile.

Business size

Business sizeAdding employees changes the cost equation across most coverage types. According to the Bureau of Labor Statistics, janitorial services recorded a total injury and illness rate of 2.5 cases per 100 workers in 2024, above the private industry average of 2.3. A window cleaning company with a two-person crew pays less than one running 10 technicians across multiple commercial accounts, where payroll size, job site count and supervisory exposure all raise costs across the board.

Location

LocationA pressure washing business operating in Louisiana pays less than an equivalent operation in Connecticut, where litigation activity, labor costs and regulatory requirements push premiums higher across most coverage types. State-level differences affect general liability and workers' comp most, but commercial auto and property coverage also vary by market.

Type of cleaning work performed

Type of cleaning work performedInsurers price cleaning trades based on the physical demands, chemical exposure and liability profile of the work. A chimney sweep working at elevation with combustion risk carries a different profile than a carpet cleaning crew working in furnished residential spaces, and those differences show up across GL, workers' comp and professional liability rates.

Vehicle use

Vehicle useCleaning businesses that run routes between job sites carry more exposure than those operating from a fixed location. According to NCCI data via the National Safety Council, motor vehicle accident claims average $91,433 per lost-time claim for accidents in 2022 and 2023. A pool cleaning company running five service vehicles daily faces a different commercial auto cost profile than a dry cleaner operating from a single storefront.

Client access and property exposure

Client access and property exposureHood cleaning services working inside commercial restaurant kitchens and air duct cleaners accessing HVAC systems in occupied office buildings carry more exposure than businesses working outdoors or in unoccupied spaces. Frequent access to client premises, high-value equipment and sensitive areas increases the probability of accidental damage, bodily injury and liability claims.

How to Lower Cleaning Business Insurance Costs

Finding cheap cleaning business insurance is possible, but some methods work within the current policy period while others take more than one renewal cycle to affect your rates.

Quick Cleaning Business Insurance Cost Lowering Methods

The following methods can produce savings at your next renewal or when you first purchase a policy.

Compare quotes using the same coverage limits

Compare quotes using the same coverage limitsRates for the same coverage vary across insurers, and cleaning businesses often see the widest spreads on general liability and workers' comp. A window cleaning company comparing quotes with inconsistent limits is effectively comparing different products. Use the same per-occurrence limit, aggregate limit and deductible across every quote to get a meaningful comparison. If you carry workers' comp, apply the same payroll basis and classification codes across all insurers to keep that comparison clean too.

Right-size your coverage

Right-size your coverageMany cleaning businesses start as solo operations and add employees, vehicles and services over time, but coverage doesn't always get adjusted to match. A maid service that scaled back from a four-person crew to two cleaners after losing a commercial contract may still be paying premiums sized for the larger operation, carrying more coverage than the current business needs. Review each policy against your current operations at every renewal.

Increase your deductible strategically

Increase your deductible strategicallyCleaning businesses often operate on thin margins, so this tradeoff requires an honest look at cash reserves. Raising your deductible lowers your premium, but only makes sense if your business can absorb the higher out-of-pocket cost after a claim. For a carpet cleaning crew with a strong claims history and a cash buffer, a higher deductible on general liability can reduce premiums without creating real financial risk.

Bundle policies with the same provider

Bundle policies with the same providerPurchasing multiple policies from one insurer often qualifies a cleaning business for a multi-policy discount. A janitorial company carrying commercial auto, general liability and commercial property with the same insurer typically pays less than one splitting those policies across three separate carriers.

Pay annually instead of monthly

Pay annually instead of monthlyMost insurers charge installment fees or apply higher effective rates to monthly payment plans. A gutter cleaning operation paying annually instead of monthly avoids those fees and pays the base premium only, which reduces the total annual cost without changing the coverage at all.

Long-Term Cleaning Business Insurance Cost Lowering Methods

Some cost reductions only show up after your claims history and risk profile have had time to shift, typically across one or more full policy periods.

Lower your risk profile

Lower your risk profileInsurers rate cleaning businesses based on the risk signals in their operations. A pressure washing business that adds a formal driver screening process, reduces vehicle use or shifts from commercial to residential accounts changes its risk profile over time, which can translate into lower commercial auto and general liability rates at renewal.

Invest in risk management practices

Invest in risk management practicesFewer claims over time directly lowers premiums across all coverage types. For cleaning businesses, the most preventable claim types (slips and falls, chemical exposure, repetitive strain and equipment injuries) are also the most common. A formal safety program that addresses these four areas can reduce claim frequency over multiple policy periods:

- Train employees on safe use, storage and disposal of cleaning agents, including which products cannot be mixed on the job.

- Require wet floor signage, non-slip footwear and clear walkway protocols at every job site, regardless of cleaning trade.

- Rotate physically demanding tasks like vacuuming and equipment carrying to reduce repetitive strain injuries across janitorial and carpet cleaning crews.

- Run pre-shift checks on ladders, pressure washers, floor buffers and powered equipment before every job to prevent mechanical failures.

Cleaning Business Insurance Cost: Bottom Line

Cleaning businesses average $293 per month in insurance costs for a minimum coverage bundle, but that figure reflects a broad mix of trades and locations.

Use these three questions to put the quote you receive into context:

- Where do you fall in the distribution? Start by locating your trade, employee count and state against the benchmarks on this page. A quote that looks high in isolation may sit exactly where expected for a janitorial operation in a high-cost state with five employees. A quote that looks low may reflect narrower coverage than your operation actually needs.

- Is your quote consistent with your risk profile? If a quote sits well above or below the benchmarks for your trade and state, that gap is worth understanding before accepting or rejecting it. A lower-than-expected quote may reflect narrower coverage limits or missing coverage types. A higher-than-expected quote may reflect how the insurer has classified your operation.

- Which cost drivers apply to your business? Not every factor carries equal weight across cleaning trades. Vehicle use matters far more for a pool cleaning route operation running five vehicles than for a laundromat with no drivers on payroll. Identify which two or three drivers actually shape your specific profile before drawing conclusions about price.

For most cleaning businesses, the gap between the industry average and an actual quote comes down to two or three factors specific to their operation, not the full list. Getting to an accurate cost picture means starting with the benchmarks that match your trade, not the ones that match the general industry.

Cleaning Business Insurance Cost: FAQ

I answer frequently asked questions about cleaning business insurance costs below:

If you're just starting out, a minimum coverage bundle that meets the most common requirements costs around $293/mo, but as your company and coverage needs grow, it can increase to an average of $559/mo.

General liability is the lowest-cost core policy in my data that can start as low as $51/mo on average, but most cleaning businesses should budget closer to $293/mo for general liability, minimum-required commercial auto coverage and a janitorial bond. This combination addresses customer injuries and property damage, driving between jobs and covered employee theft.

General liability insurance costs are the only policy that changes with cleaning business size and average $37/mo for a sole proprietorship. For a minimum coverage bundle with general liability, commercial auto and janitorial bonds, $220/mo for solo operators.

Hiring employees can add approximately $135 per month per employee for workers’ compensation based on the studied cleaning-business average, although insurers typically calculate the premium using payroll, job classifications and claims history.

Cleaning business insurance quotes vary because insurers evaluate the type of cleaning work you do, employee payroll, number of vehicles, driving records, location, property and equipment values, policy limits, deductibles and prior claims.

How We Determined Cleaning Business Insurance Costs

To estimate handyman business insurance costs, we used quotes from 10 major U.S. commercial insurance providers and modeled premiums for handyman businesses across all 50 states and Washington, D.C. The model accounts for different staffing levels, from solo handyman operations to businesses with multiple employees.

We modeled handyman premiums, not live quotes, and summarized the data in three ways:

- National benchmark average: This figure gives you a broad reference point for handyman insurance costs. It reflects standardized cleaning business profiles with one to four employees, industry-recommended policy limits and modeled results from every state and Washington, D.C.

- Profession averages: To show how profession changes cost, we compared the same base cleaner profile across 15 more specific professions, such as janitorial services, garbage collection and window cleaning.

- Bundle averages: Package costs were built from the modeled prices of individual policies, plus externally researched estimates for policies beyond our dataset.

Some cleaner add-ons fall outside the modeled dataset, including janitorial bonds, tools-and-equipment insurance, umbrella insurance and pollution liability. We used external research for these policies so you can still estimate what they add to your costs if they apply to your business.

See our full business insurance methodology and advertising disclosure for more information.

About Angelique Palenzuela-Cruz

Angelique Palenzuela-Cruz is a Business Insurance Content Writer at MoneyGeek, where she specializes in general liability, workers’ compensation and professional liability insurance. Her work helps small business owners understand how these policies apply to coverage, including risks like customer injuries, employee injuries, professional mistakes, client contract terms and industry-specific coverage requirements.

She primarily covers service-based businesses where liability and employee coverage decisions are especially important, including cleaning, consulting, beauty and wellness, childcare, education, fitness, food service, pet care, repair and maintenance, and other professional services.

Before joining MoneyGeek, Angelique spent nearly 12 years at Guthrie-Jensen Consultants, one of Southeast Asia’s largest management training firms, where she advanced from Training Consultant to Managing Consultant. In that role, she worked with business clients to assess operational needs, develop training programs and present performance analyses to executive decision-makers. She also helped establish Gladwin Training Consultancy, where she served in learning solutions and client service roles.

Her background gives her practical context for writing about how businesses operate, manage client expectations, structure teams and make risk decisions. At MoneyGeek, she applies that experience to business insurance content, connecting coverage to actual business needs.

LinkedIn: linkedin.com/in/ma-angela-cruz

Email Contact: angelique.palenzuela@moneygeek.com

Sources

- Bureau of Labor Statistics. "Table 1. Incidence Rates of Nonfatal Occupational Injuries and Illnesses by Industry and Case Types, 2024." Accessed August 11, 2026.

- Michigan Department of Insurance and Financial Services. "Frequently Asked Questions." Accessed August 11, 2026.

- National Safety Council. "Workers' Compensation Costs." Accessed August 11, 2026.