We analyzed 25 guaranteed life insurance providers and pulled thousands of quotes across different profiles to find the best guaranteed life insurance in 2026. Physicians Mutual ranks first, combining the lowest premiums in our data, a $30,000 coverage ceiling and availability to applicants as young as 45. The spread between cheapest and most expensive providers in our analysis ran $40 per month for women and $35 for men at $15,000 in coverage. That gap adds up to $480 per year for women and $420 for men with identical coverage limits and the same two-year waiting period.

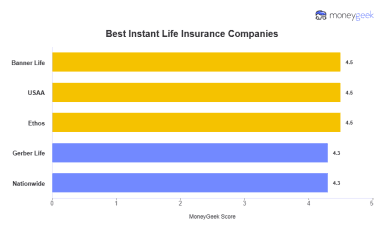

USAA is best for customer satisfaction spot with the lowest complaint index of any provider we reviewed, at 0.12. AAA, AARP, Ethos and Gerber each rank high for other unique buyer profiles.