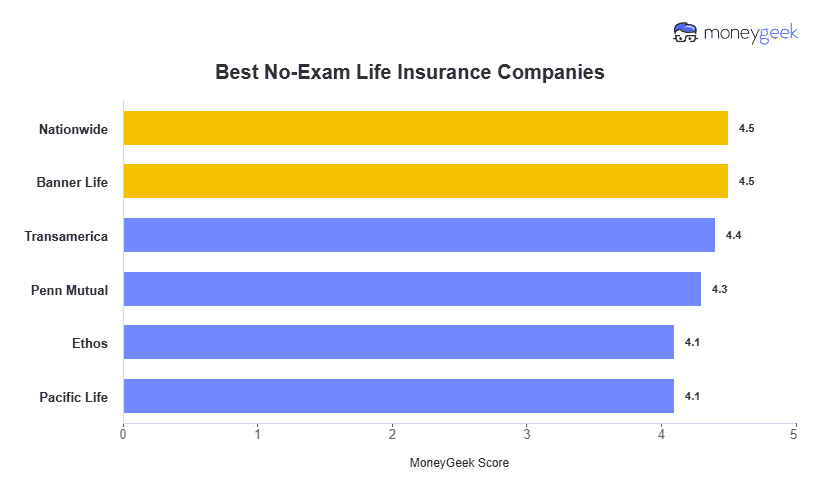

Nationwide, Banner Life and Transamerica are the best no-exam life insurance providers overall. Nationwide leads on customer experience with a 0.08 NAIC complaint index and a fully digital application for applicants ages 21 to 55. Banner Life has the cheapest rates at $41 per month for 40-year-old women and $51 for men. Transamerica accepts applicants up to age 80, the widest age range we reviewed. Penn Mutual goes up to $10 million in no-exam coverage. Pacific Life is the strongest option for smokers, covering nicotine users up to $2 million. Rates climb sharply after 50, so buying sooner lowers your long-term cost. Compare quotes from at least three providers before you buy.

Best No-Exam Life Insurance Companies (2026)

The best no-exam life insurance companies in 2026 are Nationwide, Banner Life and Transamerica.

Compare life insurance quotes from top providers.

Select age group

Updated: July 7, 2026

Advertising & Editorial Disclosure

Key Takeaways

Nationwide is the best overall no-exam life insurance company, offering up to $1.5 million in coverage, competitive rates and a fully digital application that can provide an instant approval decision.

Banner Life has the cheapest no-exam rates, averaging $41 per month for 40-year-old women and $51 for men.

Penn Mutual has the highest no-exam coverage limit at $10 million, while Banner Life has the next highest in our review at $4 million.

Pacific Life accepts smokers for up to $2 million in no-exam coverage through its Swift Sailing program.

No-exam doesn't mean no underwriting. Every insurer on this list still reviews information such as your prescription history, driving record and other available data to assess your risk. The difference is that they waive the physical medical exam, not the underwriting process.

Best Life Insurance Companies with No Medical Exam

Why You Can Trust MoneyGeek

We analyzed 30 insurance companies offering no-exam term life insurance and guaranteed acceptance whole life insurance to create our list, scoring the best options based on affordability, customer experience and coverage options. MoneyGeek maintains editorial independence and doesn't receive compensation from insurance companies for life insurance rankings or recommendations. For more information, read our full methodology.

Overall | Nationwide | $45 (F), $56 (M) | 21-55 | $1,500,000 | A+ | 4.5 |

Cheapest Rates | Banner Life | $41 (F), $51 (M) | 20-60 | $4,000,000 | A+ | 4.5 |

Seniors | Transamerica | $41 (F), $51 (M) | 18-80 | $2,000,000 | A | 4.4 |

High Coverage | Penn Mutual | $42 (F), $51 (M) | 20-65 | $10,000,000 | A+ | 4.3 |

Instant Approval | Ethos | $54 (F), $72 (M) | 20-65 | $3,000,000 | A+ | 4.1 |

Smokers | Pacific Life | $42 (F), $60 (M) | 18-60 | $3,000,000 | A+ | 4.1 |

* Rates are based on no-exam policies for 40-year-old non-smokers with $500,000 in coverage on a 20-year term. Buyers in excellent health may qualify for lower rates.

Nationwide

Best Overall

MoneyGeek Rating

4.5/ 5

4.5/5Affordability

4.8/5Customer Experience

4.2/5Coverage

Average Monthly Rate

$45 (F), $56 (M)Ages Supported

21-55Max No-Exam Coverage

$1.5 million

Banner Life

Cheapest No-Exam Life Insurance

MoneyGeek Rating

4.5/ 5

5/5Affordability

3.7/5Customer Experience

4.4/5Coverage

Average Monthly Rate

$41 (F), $51 (M)Ages Supported

20-60Max No-Exam Coverage

$4 million

Transamerica

Best for Seniors

MoneyGeek Rating

4.4/ 5

4.8/5Affordability

3.7/5Customer Experience

4.6/5Coverage

Average Monthly Rate

$41 (F), $51 (M)Ages Supported

18-80Max No-Exam Coverage

$2 million

Penn Mutual

Best for High Coverage

MoneyGeek Rating

4.3/ 5

4.7/5Affordability

3.6/5Customer Experience

4.5/5Coverage

Average Monthly Rate

$42 (F), $51 (M)Ages Supported

20-65Max No-Exam Coverage

$10 million

Ethos

Best for Instant Approval

MoneyGeek Rating

4.1/ 5

4.2/5Affordability

3.9/5Customer Experience

4.2/5Coverage

Average Monthly Rate

$54 (F), $72 (M)Ages Supported

20-65Max No-Exam Coverage

$3 million

Pacific Life

Best for Smokers

MoneyGeek Rating

4.1/ 5

4.3/5Affordability

3.6/5Customer Experience

4.5/5Coverage

Average Monthly Rate

$42 (F), $60 (M)Ages Supported

18-60Max No-Exam Coverage

$3 million

How Do No-Exam Life Insurance Companies Work?

No-exam life insurance companies let you get coverage without a medical exam. Instead of scheduling appointments with a nurse, you answer health questions online or by phone. No-exam insurers then use prescription databases, driving records and your application answers to assess risk and issue approval in days rather than weeks. Term life insurance is the most common policy type offered without an exam, but some companies like Ethos also offer whole life. No-exam policies carry higher premiums than fully underwritten coverage because insurers take on greater risk with less health data.

NO EXAM DOESN’T MEAN NO UNDERWRITING

In our review of underwriting criteria across all six providers on this list, one pattern stood out: none of these carriers actually skip underwriting. They skip the physical exam. Every provider we reviewed checks prescription drug history, motor vehicle records, and in most cases a credit-based insurance score. Nationwide's Life Essentials platform reviews all three in real time and returns most decisions instantly. Banner Life adds a health interview. Pacific Life accepts bloodwork from your doctor's office if you've had it done in the past 18 months. The "no exam" label describes the process, not the scrutiny.

No-Exam Life Insurance Pros and Cons

Weigh the benefits and drawbacks of no-exam plans before purchasing:

Pros | Cons |

|---|---|

Quick application process: Apply online or by phone and get your policy within days instead of weeks | Higher monthly costs: Insurers skip the physical exam but still assess risk through prescription records and driving history. Insurers take on more risk with less data compared to a full exam, so premiums run higher than traditionally underwritten policies. |

Simpler approval: Pre-existing medical conditions won't automatically disqualify you from coverage | Smaller death benefits: Payout amounts are lower than with fully underwritten policies |

Flexible options: Choose from various coverage amounts and policy types to match your budget and needs | Coverage caps: Most no-exam policies have lower coverage limits than traditionally underwritten policies. |

How Much Does No-Exam Life Insurance Cost?

No-exam life insurance rates rise gradually through your 30s and 40s, then accelerate sharply at 50. A female nonsmoker buying $500,000 in 20-year term coverage pays $33 per month at 20 and $50 at 40, a 52% increase over two decades. The jump from 40 to 50 is even steeper, rising from $50 to $112, a 124% increase in a single decade. Men see an even sharper climb. If you're approaching 50 and considering a no-exam policy, buying before your next birthday has meaningful rate implications that compound over a 20- or 30-year term.

20-Year No-Exam Term Life Insurance Cost

20 | $12 (F), $13 (M) | $21 (F), $24 (M) | $33 (F), $40 (M) | $46 (F), $55 (M) | $57 (F), $69 (M) |

30 | $12 (F), $14 (M) | $21 (F), $24 (M) | $33 (F), $40 (M) | $46 (F), $56 (M) | $58 (F), $71 (M) |

40 | $16 (F), $20 (M) | $30 (F), $37 (M) | $50 (F), $63 (M) | $71 (F), $91 (M) | $91 (F), $116 (M) |

50 | $32 (F), $41 (M) | $63 (F), $83 (M) | $112 (F), $149 (M) | $163 (F), $217 (M) | $210 (F), $282 (M) |

60 | $79 (F), $107 (M) | $165 (F), $226 (M) | $296 (F), $408 (M) | $438 (F), $613 (M) | $565 (F), $806 (M) |

30-Year No-Exam Term Life Insurance Cost

20 | $17 (F), $21 (M) | $31 (F), $39 (M) | $52 (F), $65 (M) | $75 (F), $98 (M) | $94 (F), $128 (M) |

30 | $19 (F), $23 (M) | $35 (F), $43 (M) | $59 (F), $72 (M) | $86 (F), $106 (M) | $110 (F), $137 (M) |

40 | $28 (F), $35 (M) | $54 (F), $68 (M) | $93 (F), $117 (M) | $137 (F), $174 (M) | $176 (F), $225 (M) |

50 | $63 (F), $82 (M) | $125 (F), $170 (M) | $218 (F), $302 (M) | $322 (F), $449 (M) | $413 (F), $580 (M) |

* These average monthly rates are based on term policies for non-smokers in average health. Buyers in excellent health may qualify for lower rates. Smokers and applicants with health conditions will pay higher premiums.

Types of No-Exam Life Insurance

No-exam life insurance falls into three categories based on how insurers evaluate your application:

- Accelerated underwriting: Insurers use algorithms to review medical records and other data instead of requiring a medical exam. Approval takes days, with higher coverage limits than simplified or guaranteed issue plans. Best for healthy applicants under 60 seeking high coverage amounts. Consider Nationwide, Banner Life, Penn Mutual or Pacific Life.

- Simplified issue: Insurers ask health questions but skip the medical exam. Coverage limits are lower than accelerated underwriting but higher than guaranteed issue. Best for people with moderate health conditions or seniors seeking smaller coverage amounts.

- Guaranteed issue: Guaranteed acceptance life insurance accepts all applicants regardless of health conditions, with no medical questions or exams required. Coverage limits are the lowest among no-exam policy types, and premiums are higher to offset the insurer's risk. Most guaranteed policies include a graded death benefit: if you pass away within the first two to three years, beneficiaries receive a return of premiums paid rather than the full death benefit. Best for applicants over 45 with serious health conditions who have been declined elsewhere.

Accelerated vs. Simplified vs. Guaranteed Issue Policies

Health questions? | Yes, detailed | Yes, brief | No |

Medical exam? | No | No | No |

Third-party data reviewed? | Yes | Yes | No |

Can you be declined? | Yes | Yes | No |

Premium vs. fully underwritten | Same cost | Higher | Much higher |

Best for | Healthy buyers under 65 | Moderate health conditions | Serious health conditions, seniors over 75 |

How to Choose the Best No-Exam Life Insurance Companies

The best no-exam life insurance company depends on your age, health profile and how much coverage you need:

Age eligibility

Age eligibilityNationwide's Life Essentials platform cuts off at 55, while Transamerica accepts applicants up to 80 years old. If you're older than 55, your provider options narrow.

Coverage limits

Coverage limitsPenn Mutual goes up to $10 million without an exam. Nationwide caps at $1.5 million. Use our life insurance coverage calculator to find your target death benefit before comparing rates.

Underwriting fallback policy

Underwriting fallback policyBanner Life and Pacific Life move declined applicants to full underwriting rather than rejecting them outright. If your health history isn't clean, that fallback matters.

Smoker eligibility

Smoker eligibilityPacific Life's Swift Sailing program covers nicotine users up to $2 million. Most competitors cap smoker coverage lower or charge rates that make other options worth comparing.

Application process

Application processNationwide and Ethos offer fully digital applications with instant decisions and same-day approvals. Pacific Life requires an agent, which adds time.

Complaint history

Complaint historyNationwide's 0.08 NAIC complaint index is among the lowest we found. Transamerica's 3.86 index means policyholders file complaints at nearly four times the industry average.

Financial strength ratings

Financial strength ratingsNationwide, Banner Life, Penn Mutual, Pacific Life and Ethos hold A+ ratings from AM Best, which measures an insurer’s financial strength and ability to pay future claims. Transamerica earned an A rating, still strong but slightly lower, which matters for policies intended to last 20 to 30 years.

Best Life Insurance Providers with No Medical Exam: Bottom Line

No-exam life insurance lets you get coverage without a doctor's appointment or medical questions. Nationwide, Banner Life and Transamerica offer the best life insurance without a medical exam today. To get the best rates, compare quotes from multiple providers.

Frequently Asked Questions

Understanding the differences between traditional life insurance policies and those that don't require a medical exam is challenging. Get answers to some of the most frequently asked questions to help you determine if a life insurance policy with no medical exam is right for you:

Nationwide is the best overall no-exam life insurance company based on affordability, customer service and its digital application process. Its 0.08 NAIC complaint index is among the lowest in the category. Banner Life has the cheapest rates, with average monthly premiums of $41 for women and $51 for men at 40 years old with a $500,000 policy.

Whether you need an exam depends on the policy type. Accelerated underwriting skips the physical exam but still reviews prescription history and driving records. Guaranteed issue skips both the exam and health questions. Traditional underwriting includes a full exam but offers lower premiums and higher coverage limits for healthy buyers.

You can be denied life insurance even without a medical exam. Insurance companies review your application, medical history, prescription records and conduct phone interviews. They may deny coverage based on serious health conditions, risky occupations, dangerous hobbies or incomplete application information.

No-exam life insurance works well for healthy buyers who need coverage quickly. Premiums run $12 to $17 per month higher than fully underwritten policies for a 40-year-old buying $500,000 in coverage. That cost difference is worth it for buyers who want same-day approval or want to avoid scheduling a medical exam.

Learn more: Is Life Insurance Worth It?

No-exam life insurance uses accelerated underwriting, reviewing medical records, prescription history and application answers instead of requiring a physical exam. Traditional underwriting includes blood tests, urine samples and physical examinations. No-exam policies offer faster approval, typically days versus weeks, but carry lower coverage limits and higher premiums.

Instant life insurance uses automated underwriting to approve applications within minutes to 48 hours without a medical exam. Applicants answer basic health questions online, and algorithms analyze health records and data to make immediate coverage decisions. Approval can happen the same day, though death benefit payouts still require standard claim processing.

Our Methodology

Our Research Approach

No-exam life insurance appeals to people who need fast coverage or have health conditions that make traditional underwriting difficult. Because premiums run higher and coverage limits may be lower, choosing the right insurer matters for long-term financial protection.

We analyzed 30 providers offering no-exam term life and guaranteed acceptance whole life policies. Our evaluation considered premium quotes, customer satisfaction, financial strength and product features to identify the best options.

How MoneyGeek scored each insurer:

- Affordability (50%): Premium costs matter most when insurers skip medical underwriting. You'll pay more without an exam, and those differences multiply over ten, 20 or 30 years. MoneyGeek collected thousands of quotes for all reviewed companies to identify the most competitive rates across different age, term, coverage level, smoking habit and health profiles.

- Customer Experience (30%): Claims processing speed and service quality determine whether your beneficiaries get paid promptly. Customer feedback, J.D. Power ratings and complaint data from state insurance departments revealed which insurers deliver reliable support.

- Coverage Options (20%): No-exam policies typically cap coverage lower than traditional term life and restrict rider availability. Product variety, policy customization and maximum coverage amounts separated flexible insurers from limited ones.

Read more in our full Life Insurance Methodology.

Related Pages

About Patrick Bryant

Patrick Bryant is the Vertical Lead for Life and Health Insurance at MoneyGeek, where he researches insurance products, writes consumer guides and maintains the scoring methodologies behind our provider comparisons. He analyzed more than 50 life insurance carriers across multiple policy types, collecting thousands of quotes nationwide to evaluate rates, coverage options and underwriting factors. His methodologies are reviewed quarterly to reflect current market conditions and carrier data.