GEICO is the cheapest liability only insurer nationally at $43 per month, 35% below the national average of $67. Travelers and National General are both affordable at $50 per month but serve very different driver profiles. National General is the right starting point for drivers with violations or non-standard risk profiles that standard insurers decline to quote. Travelers balances affordability with the ability to speak with an agent to buy your policy.

Cheapest Liability-Only Car Insurance

Updated: June 4, 2026

Advertising & Editorial Disclosure

Low-Cost Liability Car Insurance: MoneyGeek's Take

GEICO has the cheapest liability only car insurance at $43 per month, 35% below the national average. In our analysis the gap between the cheapest and most expensive insurer for the same driver profile is $216 annually, making insurer selection more impactful than most drivers expect.

Liability only is the cheapest legal option but does not cover damage to your own vehicle after an at-fault accident, theft or weather damage. It makes sense for drivers on a very tight budget or those with low value vehicles.

Why You Can Trust MoneyGeek for Car Insurance

We analyzed 2,474,515 liability car insurance quotes from 607 insurance providers across 3,523 ZIP codes to create our cheapest liability-only car insurance rankings. Mark Fitzpatrick, a licensed insurance professional and industry analyst, reviewed our methodology. We update our liability car insurance data and rankings monthly to keep them current.

MoneyGeek maintains editorial independence and doesn't receive compensation from insurance companies for our rankings or recommendations.

Cheapest Liability-Only Car Insurance

Data filtered by:

Male

Adult Drivers

Clean

Good

| Geico | $43 | $522 | 35% |

| Travelers | $50 | $601 | 25% |

| National General | $50 | $605 | 25% |

| State Farm | $51 | $616 | 24% |

| Amica | $56 | $669 | 17% |

| Chubb | $61 | $728 | 10% |

| Kemper | $62 | $744 | 8% |

GEICO

Cheapest Liability Car Insurance Company: GEICO

GEICO is our top pick for cheapest liability only coverage at $43 per month and earns the highest affordability score in our best car insurance companies analysis. One thing worth knowing before you default to it: GEICO scores below the industry average on J.D. Power claims satisfaction. For a driver who rarely files claims and wants the lowest possible bill it is the right call. For a driver who values support after an accident, the $7 monthly difference to State Farm or Travelers is worth considering.

Summary of Cheapest Liability By Driver Profile

Not every driver gets the cheapest liability rate from the same insurer. Use the chart below to match your driving profile and find which company is the cheapest for you.

Cheapest Liability-Only Car Insurance Quotes by Age

Liability rates vary across age groups. Teens pay two to three times the adult rate due to high accident frequency. Rates drop steadily through the 20s, reach their lowest point for drivers in their 50s and 60s and rise again after 65. The cheapest liability-only insurer shifts by age group, which is why a national average rate is rarely useful for drivers at either end of the age range.

Cheapest Liability-Only Insurance for Young Drivers

National General is the cheapest insurer for young drivers aged 16-24 at $101 per month, 37% below the national average for this age group. GEICO's rate is similar at $105 per month.

National General leads on price but has an NAIC complaint index of 3.17, meaning significantly more customer complaints than its industry peers. For young drivers, GEICO's $4 monthly difference buys meaningfully better service and a fully digital experience that makes policy management straightforward.

Staying on a parent's policy is almost always the right call for drivers under 25 as long as you live at the same address. Families save 10 to 60 percent compared to a standalone policy for the same young driver depending on the age of the driver.

| National General | $101 | $1,211 | 37% |

| Geico | $105 | $1,265 | 34% |

| Travelers | $116 | $1,391 | 27% |

| State Farm | $117 | $1,407 | 26% |

| Amica | $133 | $1,594 | 17% |

*Rates are based on adding a teen or young adult (Age 16–24) to a parent's established policy.

Cheapest Liability-Only Car Insurance for Seniors

GEICO has the cheapest liability only car insurance for seniors at $56 monthly, 35% below the $87 senior average. We found that GEICO leads on price but scores below Amica and State Farm on on claims satisfaction. State Farm at $62 is worth the extra $6 per month for seniors who want a local agent and a more hands-on claims experience.

Senior rates rise after 65 due to higher accident frequency, but those who take advantage of senior discounts with clean records and low annual mileage can offset those increases. GEICO's DriveEasy and Progressive's Snapshot both reward low-mileage drivers with rate reductions and are worth enrolling in if your annual driving has decreased in retirement.

| Geico | $56 | $673 | 35% |

| Amica | $62 | $744 | 28% |

| State Farm | $62 | $746 | 28% |

| National General | $67 | $807 | 22% |

| Travelers | $70 | $838 | 19% |

Cheapest Liability-Only Car Insurance Quotes by State

GEICO offers the cheapest liability only coverage in 13 states averaging $36 per month and State Farm leads in nine states at $28 per month. Regional insurers beat both in the remaining states. Farm Bureau, Westfield and other local insurers price regional risks.

The percent difference column in the table below tells you how much comparison shopping pays off in your state. In Alabama the cheapest insurer is 60 percent below the state average, meaning there is a clear winner and finding it saves more money. In other states that gap is smaller, meaning most insurers price similarly and switching insurers means less savings.

| Alabama | AIG | $22 | $268 | 60% |

| Alaska | Geico | $40 | $481 | 14% |

| Arizona | Travelers | $45 | $546 | 34% |

| Arkansas | Farm Bureau | $32 | $383 | 34% |

| California | Geico | $39 | $465 | 43% |

| Colorado | American National | $27 | $326 | 54% |

| Connecticut | Geico | $35 | $419 | 60% |

| Delaware | Travelers | $46 | $551 | 57% |

| District of Columbia | Chubb | $29 | $352 | 70% |

| Florida | Travelers | $51 | $617 | 46% |

| Georgia | Geico | $42 | $498 | 48% |

| Hawaii | Geico | $24 | $292 | 32% |

| Idaho | State Farm | $18 | $210 | 52% |

| Illinois | Geico | $31 | $368 | 40% |

| Indiana | Hastings Insurance | $30 | $364 | 27% |

| Iowa | State Farm | $19 | $231 | 42% |

| Kansas | Geico | $26 | $309 | 45% |

| Kentucky | Travelers | $47 | $560 | 40% |

| Louisiana | Geico | $55 | $659 | 48% |

| Maine | MMG Insurance | $27 | $330 | 29% |

| Maryland | Geico | $49 | $586 | 45% |

| Massachusetts | Plymouth Rock Insurance | $22 | $267 | 51% |

| Michigan | Travelers | $23 | $277 | 64% |

| Minnesota | Westfield Insurance | $19 | $231 | 57% |

| Mississippi | Farm Bureau | $33 | $402 | 42% |

| Missouri | Auto Owners | $34 | $402 | 47% |

| Montana | State Farm | $18 | $220 | 63% |

| Nebraska | Farmers Mutual Ins Co of NE | $18 | $216 | 55% |

| Nevada | Travelers | $57 | $686 | 31% |

| New Hampshire | Safety Insurance | $31 | $371 | 31% |

| New Jersey | Plymouth Rock Insurance | $67 | $806 | 34% |

| New Mexico | Central Insurance | $31 | $368 | 40% |

| New York | NYCM Insurance | $25 | $305 | 60% |

| North Carolina | State Farm | $24 | $289 | 52% |

| North Dakota | North Star Insurance | $25 | $295 | 40% |

| Ohio | Auto Owners | $27 | $318 | 38% |

| Oklahoma | Progressive | $28 | $331 | 50% |

| Oregon | State Farm | $38 | $455 | 32% |

| Pennsylvania | Westfield Insurance | $20 | $234 | 61% |

| Rhode Island | State Farm | $42 | $500 | 43% |

| South Carolina | American National | $34 | $413 | 50% |

| South Dakota | Farmers Mutual Ins Co of NE | $13 | $157 | 60% |

| Tennessee | Farm Bureau | $27 | $319 | 45% |

| Texas | State Farm | $41 | $489 | 41% |

| Utah | Geico | $48 | $573 | 33% |

| Vermont | Co-operative Insurance | $16 | $189 | 48% |

| Virginia | Travelers | $30 | $365 | 43% |

| Washington | State Farm | $37 | $442 | 30% |

| West Virginia | Westfield Insurance | $30 | $362 | 47% |

| Wisconsin | Geico | $21 | $249 | 44% |

| Wyoming | Geico | $14 | $169 | 47% |

Here are our guides for deeper research on the cheapest liability car insurance rates in your state:

Cheapest Liability-Only Car Insurance With Violations

A violation does not mean you are stuck overpaying. In our analysis the gap between the most and least forgiving insurer after a single at-fault accident is $400 per year for the same driver. The insurer that is cheapest with a clean record is rarely the cheapest after a violation, which is why shopping after any incident is worth the effort.

State Farm is the cheapest for drivers with most violations while GEICO is the lowest cost for distracted driving and not-at-fault accidents. Here is what our data shows by violation type:

- At-fault accident: State Farm offers the most affordable liability coverage after an at-fault accident at $62 per month, 34% below the high-risk average. Most at-fault accidents stay on your record for three to five years.

- Speeding ticket: State Farm also has the cheapest rates after a speeding ticket at $56 per month. Most moving violations impact your rate for three to five years.

- Texting while driving: GEICO is the most affordable option after a distracted driving ticket at $55 per month. In our research insurers vary more on how they price texting violations than almost any other incident type.

- DUI conviction: State Farm offers the lowest rates after a DUI at $73 per month. DUI offenses stay on your record for three to 10 years and often require an SR-22 filing. Drivers with a suspended license and no vehicle may need non-owner car insurance.

- Not-at-fault accident: GEICO is cheapest at $45 per month. Most insurers still raise rates after a not-at-fault accident and GEICO keeps that increase lower than most competitors.

Most violations fall off your record after three to five years and your rate drops at each renewal as they age off. A DUI typically takes five to seven years to fully clear depending on your state, while a speeding ticket or at-fault accident usually stops affecting your rate after three years.

Cheapest Liability Car Insurance for Drivers with Bad Credit

National General is the cheapest insurer for drivers with poor credit at $61 per month, with GEICO one dollar behind at $62. The decision comes down to claims experience rather than price. National General carries an NAIC complaint index of 3.17, more than three times the industry average. GEICO's complaint index is well below average, its app handles most policy needs without a call and it scores higher on customer satisfaction across every profile we analyzed.

Poor credit raises liability premiums by 34% or more in most states, making it one of the largest rate factors outside of a DUI. California, Hawaii and Massachusetts prohibit credit-based pricing entirely, so drivers in those states pay the same rate regardless of credit history. Everywhere else, moving from poor to good credit cuts premiums by $20 to $50 per month without changing your coverage or carrier, making credit improvement one of the best ways to save.

Data filtered by:

Adult Drivers

Clean

Fair

| National General | $61 | $736 | 34% |

| Geico | $62 | $740 | 34% |

| Travelers | $75 | $895 | 20% |

| Kemper | $75 | $905 | 19% |

| Amica | $87 | $1,046 | 6% |

Cheapest Liability Car Insurance for Military Members

USAA is the cheapest insurer for active duty military, veterans and their eligible family members at $28 per month, 47% below the national average. GEICO is the strongest alternative. It offers a dedicated military discount cuts 12 to 15 percent off the base rate and it has a dedicated military customer service team staffed with veterans available 24 hours a day. In our analysis GEICO's effective rate after the military discount is often competitive with or cheaper than non-military specialized carriers for this profile.

| USAA | $28 | $335 | 47% |

| National General | $48 | $580 | 15% |

| Travelers | $50 | $597 | 21% |

| Amica | $57 | $683 | 6% |

How to Get Cheaper Liability-Only Car Insurance

In our analysis of liability rate factors, these six strategies produce the most consistent savings on liability only policies.

- 1Match your profile to the right insurer

GEICO and State Farm have the cheapest minimum liability nationally but the cheapest option for your specific age, credit score and driving record may be different. Get quotes from at least three insurers including regional options in your state. Use our car insurance calculator to estimate costs before requesting formal quotes and our insurer reviews to evaluate service quality alongside price.

- 2Understand What State Minimum Liability Actually Covers

Most states require only $25,000 to $50,000 in bodily injury liability per person. A single serious accident can exceed that in medical bills alone, leaving you personally responsible for the difference. Before choosing state minimums, consider your assets. If you own a home or have savings worth protecting, carrying higher limits costs $5 to $20 more per month and is better protection for your assets. See our guide to how much car insurance you need.

- 3Stack every discount where you qualify

Take advantage of every discount you qualify for. These directly lower your final premium:

- Bundle Discounts: Combine auto with renters or home insurance for savings up to 25%.

- Safe Driver Rewards: Maintain a clean driving record to qualify for discounts and eliminate accident/violation surcharges.

- Low Mileage: Qualify for reduced rates if your annual driving is low (under 7,500 miles).

- Affinity Discounts: Check for membership savings if you belong to a military, professional or alumni organization.

- Pay in Full: Pay your entire premium upfront (annually or semi-annually) for a 5% to 10% discount.

- Multi-car insurance: Multiple cars under the same policy save on your rate.

- 4Improve your credit score

In most states poor credit nearly doubles your liability premium. Improving your score is one of the most effective long-term ways to lower your rate without changing your coverage or carrier.

- 5Enroll in a Telematics Program

GEICO's DriveEasy and Progressive's Snapshot track your driving through an app and reward safe behavior with discounts of 15% to 40%. Both offer an immediate discount just for enrolling. DriveEasy works best for low-mileage drivers. Snapshot is the stronger option for drivers with a prior violation who want a concrete path to lower rates over time. Neither program penalizes you for occasional hard braking, but aggressive driving can raise your rate at renewal.

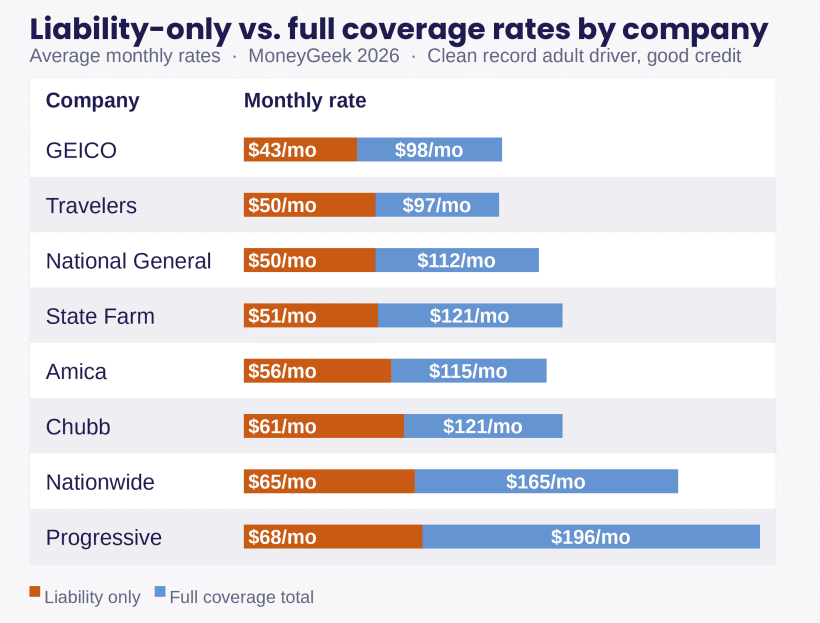

Is Liability-Only Car Insurance the Right Choice?

We get it, car insurance is expensive and liability-only coverage is cheaper than full coverage. See the table below to see the difference in coverage between the two.

Covers injuries you cause to others | ✓ | ✓ |

Covers damage you cause to others' property | ✓ | ✓ |

Covers damage to your own vehicle | — | ✓ |

Covers theft of your vehicle | — | ✓ |

Covers weather, fire, vandalism | — | ✓ |

Required by lenders on financed vehicles | — | ✓ |

Average monthly cost | $43–$68 | $97–$196 |

It works best when your car is paid off and worth less than $5,000. At that point the annual cost of comprehensive and collision (full coverage) is expensive to insure a low value car. See our guide to how much car insurance you need.

As Mark Friedlander of the Insurance Information Institute puts it: "Liability only coverage leaves drivers financially responsible when it comes to their own vehicle. If you cause an accident and cannot afford to repair or replace your car out of pocket, full coverage is worth the extra cost."

If you are financing or leasing, liability-only is not an option. Your lender requires full coverage and if you drop it they will force-place insurance at two to three times the cost.

Here is the comparison of liability-only cost vs full coverage.

Cheap Liability-Only Car Insurance: FAQ

Below are some frequently asked questions and answers about liability-only car insurance:

Does liability only cover me if someone hits me?

No. Liability only covers damage and injuries you cause to others. If another driver hits you and they are uninsured or underinsured, you have no coverage for your own vehicle or injuries unless you carry uninsured motorist coverage. This is one of the most common gaps we see in liability only policies and one of the strongest arguments for adding uninsured motorist coverage even if your state does not require it.

Is liability only insurance legal in every state?

Yes. Every state allows liability only coverage as long as it meets the state minimum requirements. New Hampshire and Virginia are the only states that do not require drivers to carry insurance at all, though financial responsibility is still required if you cause an accident.

Why do some states require coverages like PIP and UM/UIM with a "minimum liability" policy?

Some states require coverage beyond standard Bodily Injury and Property Damage Liability to ensure financial protection for you and your passengers:

- Personal Injury Protection (PIP): Required in "no-fault" states (e.g., Florida, New York) to cover your own medical bills and lost wages, regardless of who caused the crash.

- Uninsured/Underinsured Motorist (UM/UIM): Required in about half of states to protect you if an at-fault driver has no insurance or insufficient insurance limits to cover your damages.

Loading...

Our Methodology

We designed this research to identify the most accessible liability coverage options without sacrificing accuracy.

Data Collection

Our team gathered 2,474,515 quotes from 607 insurance companies in 3,523 ZIP codes nationwide. We got this information directly from state insurance departments and Quadrant Information Services, then compared the actual prices people pay.

Sample Driver Profile

We calculated average annual car insurance rates using this sample driver profile:

- 40-year-old male driver

- Driving a Toyota Camry LE

- No on-record violations

- Good credit score

- Clean driving record with no claims history

We adjusted this profile by age, driving record, credit score and car type to get rates for different driver types, including high-risk profiles with violations and drivers with poor credit. See our full methodology.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident insurance expert. He has spent nearly a decade analyzing the market, first at LendingTree and now at MoneyGeek, where he produces original research on hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

He covers economics and insurance at MoneyGeek, and his work has been featured in The Washington Post, The New York Times and NPR, among other outlets.

Like all MoneyGeek analysts, he draws on independent cost and consumer experience data. No insurance company partnership influences his recommendations.

Fitzpatrick earned his degrees from Johns Hopkins University (M.A. Economics and International Relations) and Boston College (B.A.). His career began in financial risk management at State Street. He's also a five-time “Jeopardy!” champion.