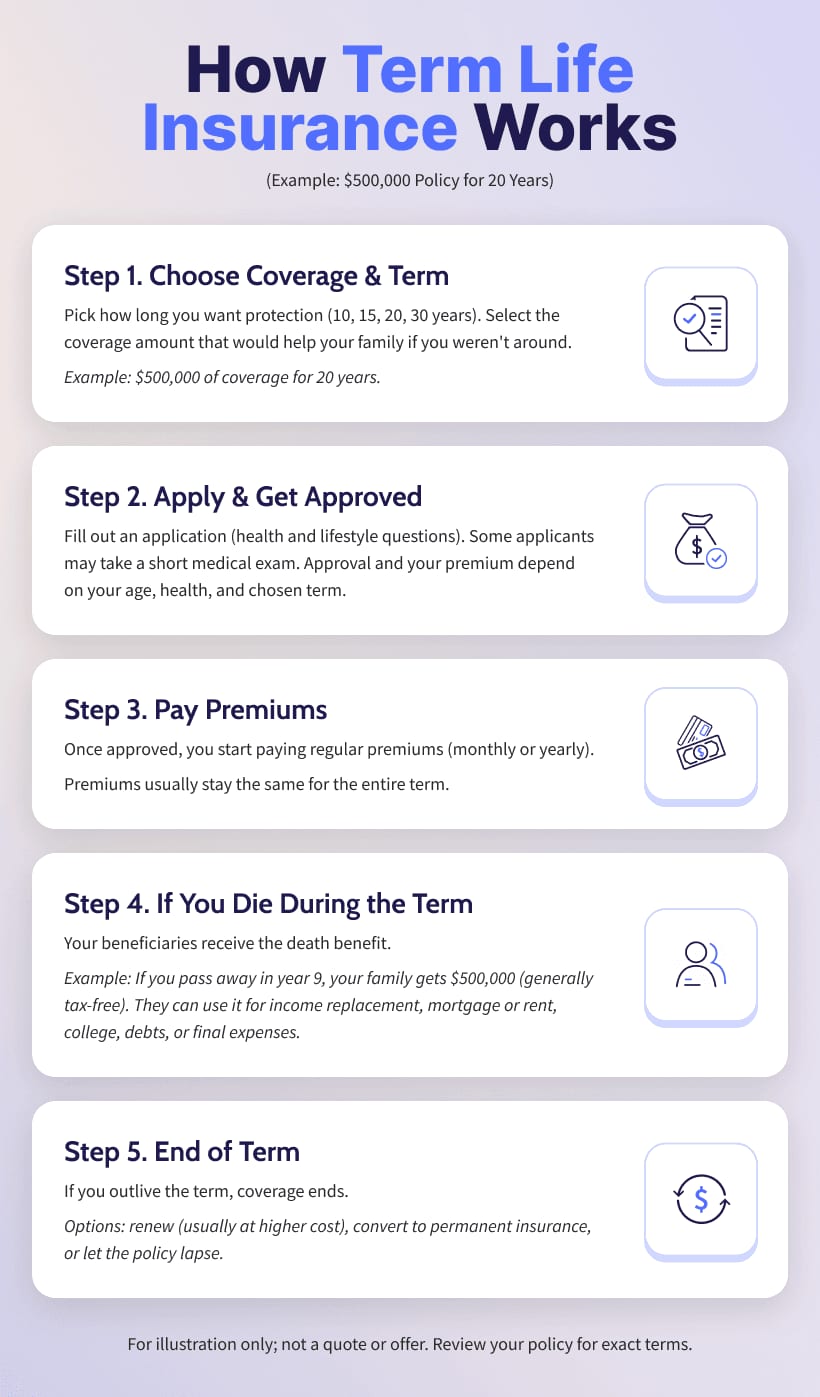

Term life insurance provides financial protection for your family or dependents at a specified coverage amount (called the death benefit) for a set timeframe.

This makes term life insurance the most affordable type of life coverage. You pay a fixed monthly or annual premium, and if you die during the term, your family gets the full death benefit. If you outlive the policy term, coverage ends and you won't get money back.