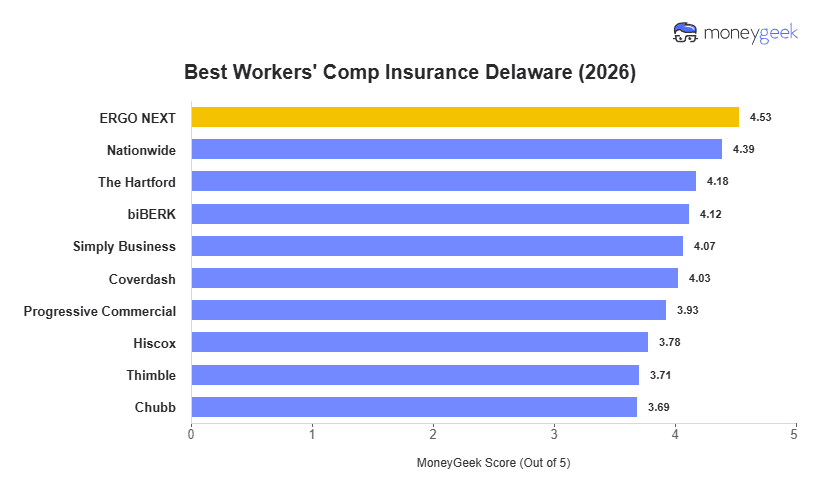

ERGO NEXT has the best worker's comp insurance in Delaware with the state's lowest monthly rate at $91 alongside our highest customer experience ranking. Nationwide ranks second at $100/month with the second-strongest affordability score in the state.

The $81 spread between ERGO NEXT ($91/month) and Chubb ($172/month) is meaningful for Delaware's professional and service-sector businesses. The gap narrows in construction and logistics class codes, where base loss costs converge upward across all carriers.