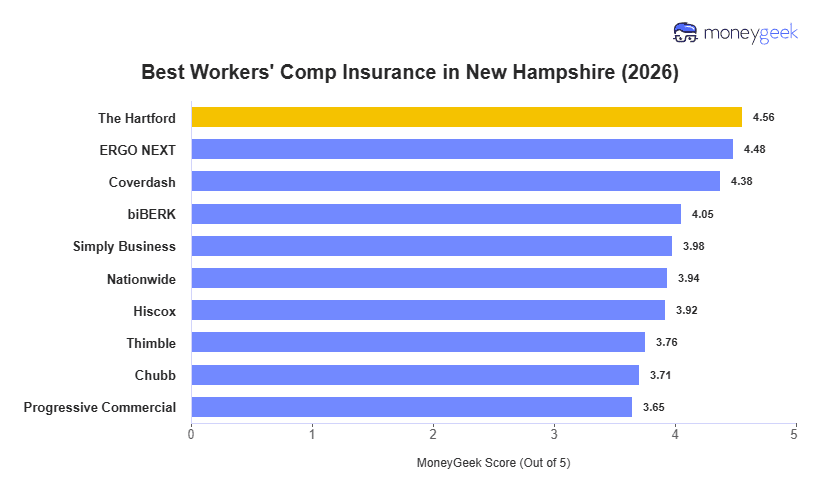

The Hartford is the best workers' compensation insurance provider in New Hampshire with an average monthly rate of $89 per employee. ERGO NEXT also averages $89 monthly but ranks second overall, leading all providers in customer experience. Coverdash ranks third at $105 per month and leads in coverage quality, making it a strong option for businesses that prioritize plan depth over cost.

The $64/month gap between The Hartford and Chubb ($153) average monthly rates translates to $768/year per employee for New Hampshire businesses. The pricing gap widens for construction and logging employers where high-hazard class code rates amplify the base difference.