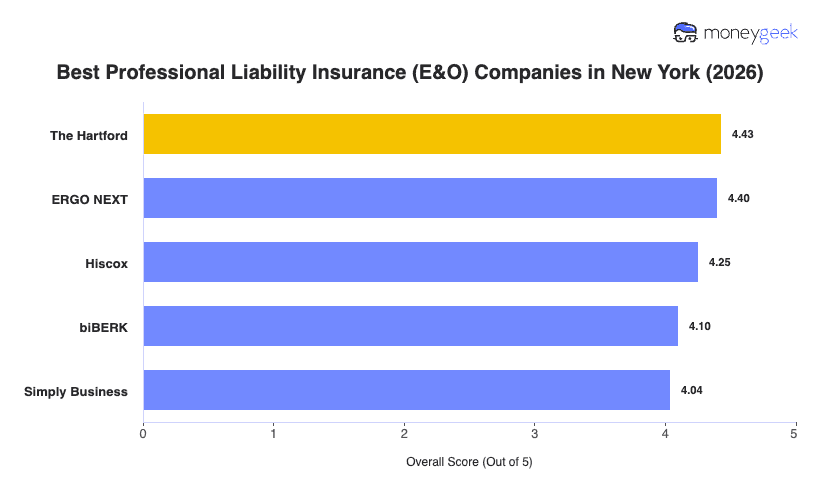

Our analysis of New York professional liability insurers found three providers that consistently outperformed the field across affordability, customer experience and coverage quality.

- The Hartford: Ranking at the top spot for New York, it leads on affordability across more industries than any other provider in the state, placing first in eight categories including consulting, financial services, tech/IT, marketing and hospitality. The insurer has over 200 years in the business and covers professional liability claims online 24/7, with customer service available by phone Monday through Friday from 8 a.m. to 8 p.m. EST. New York businesses in healthcare and other professional services categories should note that The Hartford ranks lower in those industries and may find a better fit elsewhere.

- ERGO NEXT: A strong second overall, the insurer ranks first in nine New York industries including construction and contracting, fitness services, pet care, nonprofit and associations, healthcare and medical, and recreation and sports. Its fully digital buying experience lets New York businesses complete a policy in under six minutes and access certificates of insurance instantly through its app or website, without requiring an agent. ERGO NEXT does not extend professional liability coverage to certain higher-risk operations, so verify your industry's eligibility before purchasing.

- Hiscox: Third overall, Hiscox earns its spot through deep specialization in professional services, with tailored policies across more than 180 industries and professional liability coverage that extends globally for work performed outside the U.S. as long as claims are filed domestically. Its online quote process requires no agent call and produces a certificate of insurance within about 15 minutes. New York financial services and consulting businesses can also benefit from its strong rankings in those categories.

These three providers represent the best fit for most New York businesses, but no ranked list covers every profession, firm size or risk profile. Comparing business insurance options side-by-side and getting direct quotes gives you the clearest picture of what fits your business.