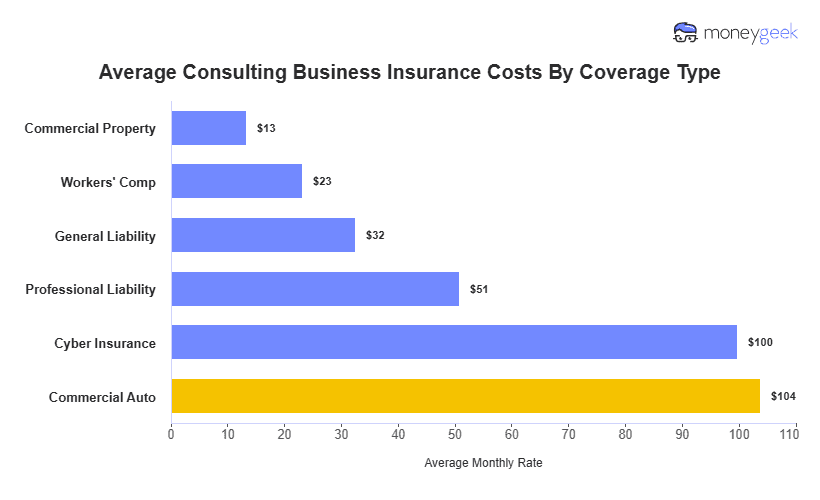

The average cost of business insurance for consulting services range from $54 monthly ($646 annually) across six coverage types. This figure is from our analysis of estimates for businesses with one to four employees across 50 states and Washington, D.C., reflecting the full range of policies a consulting firm might carry, not the cost of any single policy.

Individual coverage types range from $13 to $104 monthly, with specialty, employee count, and coverage mix all driving what a firm actually pays. Commercial property sits at the low end because many consultants run lean offices with limited equipment, while professional liability and cyber insurance cost more because client advice, data handling and digital workflows create higher-risk exposures.

The table below shows average monthly and annual costs by coverage type. Treat these as reference points rather than quotes, since actual premiums vary by business profile.