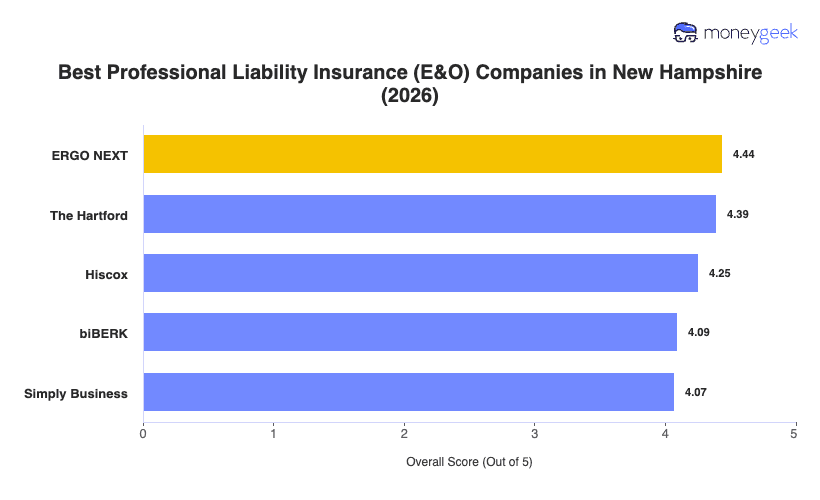

Our analysis of New Hampshire professional liability insurers found three providers that consistently outperformed the field on rates, coverage and customer experience across the state's industries.

- ERGO NEXT: Rates that undercut the New Hampshire state average combined with a fully digital buying experience that lets you quote, bind and pull certificates of insurance without talking to anyone earned ERGO NEXT the top spot. The insurer ranks first in NH across industries including construction, healthcare, fitness, recreation, arts and marketing. It's backed by Munich Re through its ERGO Group parent, which added significant financial depth when the acquisition closed in 2025. New Hampshire contractors and healthcare service businesses get the strongest fit here.

- The Hartford: Strong affordability is the headline, but what actually sets The Hartford apart for NH businesses is how well it performs across white-collar service industries. It ranks first in the state for tech, consulting, financial services, real estate and hospitality. For a Portsmouth accountant or a Manchester financial advisor shopping for E&O, The Hartford's combination of rate competitiveness and profession-specific coverage depth is hard to beat. The tradeoff: professional liability quotes require a phone call rather than a fully online process, so expect a longer buying timeline than ERGO NEXT.

- Hiscox: Over a century of specialty insurance experience and a product line built around professional services firms makes Hiscox a natural fit for New Hampshire businesses that need more coverage depth than a standard E&O policy provides. It ranks first in the state for nonprofits and puts up strong numbers for consulting, financial services and childcare. Its E&O policy forms are generally broader than what mass-market carriers offer, which matters for complex or client-contract-heavy businesses in Concord or Portsmouth.

Ranked providers represent the best fit for most New Hampshire businesses, but no single list accounts for every profession, revenue level or risk profile. Comparing business insurance options side by side and getting direct quotes gives you the clearest picture of what you'll actually pay.