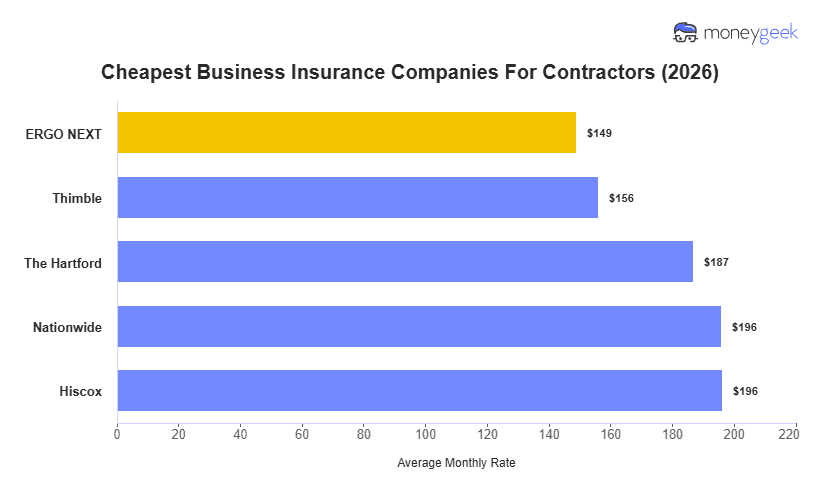

The cheapest small business insurance overall for contractors comes from ERGO NEXT, which offers average rates of $149/mo, roughly 22% below the industry average. To find the most affordable options, I analyzed business combinations in the industry across all 50 states (including DC) and 45 contractor sub-industries for a 1-to-4-person business. While they are the most affordable company overall, where you'll get the most savings will vary widely depending on your specific company's profile.

The following 5 cheapest contractor insurance companies from my research should be used as a starting point in your search, not a final answer.