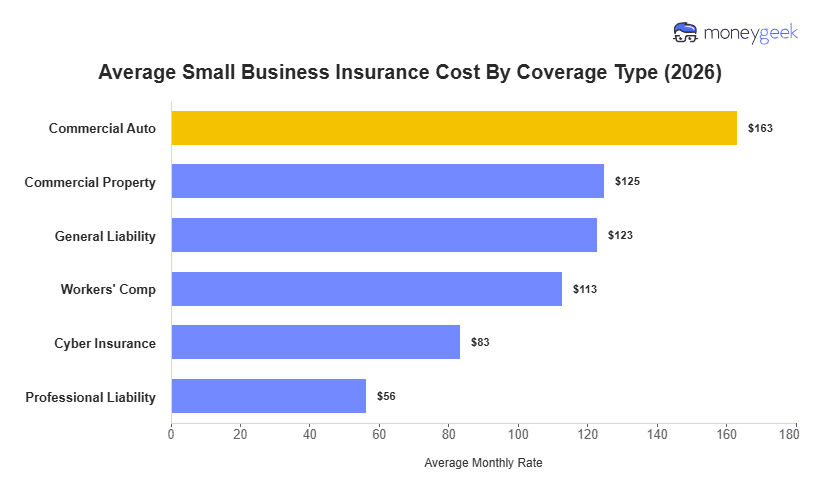

At a high level, small business insurance costs average $111 nationally across the six most common coverage types. Most small businesses start with either a general liability policy ($123/mo on average) or a BOP (Business Owners Policy) that which bundles general liability, commercial property, and business interruption at $221/mo. If you also need state mandated coverage, commercial auto adds $152/mo and workers' comp adds $99/mo per employee on top of that if you are hiring.

However, these prices are only national average benchmarks for a 1-to-4-employee business and what you'll pay will depend mainly on your coverage needs, industry, state, business size and vehicle type (if needing auto coverage). Most businesses will also sit below these averages due to higher risk industries like construction, healthcare, and transportation skewing nationwide pricing estimates higher.

To give you a more representative high-level look at costs at the coverage level, I've broken down average costs and a monthly cost range that most small businesses fit within.