The best car insurance company comes down to one question most comparison sites skip: best for whom? I've studied rates and car insurance features for over a decade, and this year's winners span a wider range of carrier types than in prior years. No single car insurance company is best for every driver; the best choice depends on your profile.

Best Car Insurance Companies for 2026

Updated: June 22, 2026

Advertising & Editorial Disclosure

Our Experience After Reviewing 70+ Car Insurers

Travelers: Top-Rated Car Insurance Company

Travelers: Top-Rated Car Insurance CompanyTravelers has the top overall score with high ratings across affordability, coverage and customer service. It ranks second nationally for rates and second for claims experience among national carriers. Coverage options include new car replacement that most carriers either don't offer or cap at two years. But Travelers doesn't offer online purchasing. You'll need to go through an agent, which rules it out for buyers who want a fully digital experience.

GEICO: Best Affordable Car Insurer

GEICO: Best Affordable Car InsurerGEICO is the best option when price is your primary decision factor. No national carrier competes with $43 a month for minimum coverage or $98 for full coverage. Claims service reviews are mixed, with some customers reporting longer phone hold times. Add-on options are fewer than other carriers in the top five, so don't choose GEICO if you have a complex coverage need. For clean-record drivers who rarely file claims and want the lowest possible monthly bill, it's the best choice.

Amica: Best for Customer Service

Amica: Best for Customer ServiceAmica is the right carrier for anyone who has had a bad claims experience somewhere else. It has the highest agent service scores of any national insurer we rated, and customer reviews back that ranking up across every platform we checked. The rates are higher than Travelers' and GEICO's. Drivers who want reliable claims handling will find the cost difference worth it. Amica calls itself a regional carrier but writes policies in 49 states; Hawaii is the only state it doesn't cover.

Progressive: Best for Coverage Options and High-Risk Drivers

Progressive: Best for Coverage Options and High-Risk DriversProgressive has the best coverage options: seven add-ons, including a Deductible Savings Bank, custom parts and equipment coverage for modified vehicles and a Snapshot telematics program that lowers rates for low-mileage drivers. The base rates run higher than the top three, but drivers with violations or bad credit will find better rates at Progressive than at any other carrier in our top five. For modified cars, rideshare drivers or anyone with a DUI or at-fault accident on record, price Progressive first.

State Farm: Best for Young Drivers and Families

State Farm: Best for Young Drivers and FamiliesState Farm is the best option for young drivers and households that want a personal agent relationship. Steer Clear and the good student discount stack together in a way no other carrier matches for drivers under 25. The agency-only model rules out State Farm for drivers who want to manage everything online. For families with teen drivers who want a local agent to handle their policy, it's the right call.

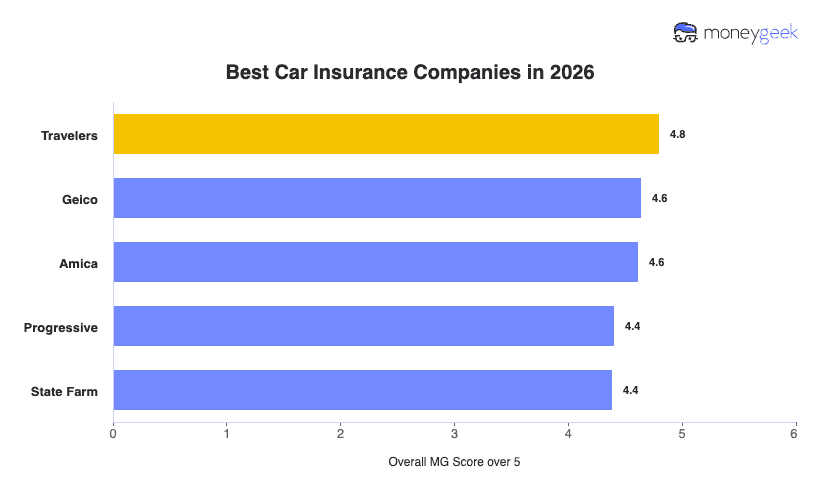

Best Car Insurance Companies: Scores and Methodology

| Travelers | 4.8 | 2 | 2 | 4 |

| GEICO | 4.64 | 1 | 7 | 7 |

| Amica | 4.61 | 4 | 1 | 5 |

| Progressive | 4.4 | 7 | 4 | 2 |

| State Farm | 4.38 | 5 | 5 | 7 |

The scores are close, but the strengths behind them aren't:

- Travelers vs. GEICO: 0.16 points apart, opposite profiles. Travelers holds its own in all three categories. GEICO wins only on price.

- Amica vs. Progressive: Nearly identical overall scores, but different strengths: Amica leads in service, Progressive in coverage.

- Progressive vs. State Farm: 0.02 points apart. Progressive leads in coverage, while State Farm edges ahead on affordability.

Best Car Insurance Company Ratings

Each of the top five carriers excels in different areas. The scoring below breaks down pricing by driver profile, customer service performance and unique coverage features for each company.

Travelers

Best for Most Drivers

MoneyGeek Rating

4.8/ 5

4.9/5Affordability

4.8/5Customer Experience

4.1/5Coverage Points

Average Monthly Full Coverage Rate

$97Based on our methodology's base profile for a 100/300/100 liability and $1,000 deductible comprehensive and collision policyAverage Monthly Minimum Coverage Rate

$50r methodology's base profile for a state minimum liability coverage policy.Agent Service Rating

4.2/5Aggregated from ratings for independent and captive agents representing and selling Travelers car insurance policiesUnique Coverage Option

New car replacement

GEICO

Best Cheap Car Insurance

MoneyGeek Rating

This score was determined with a split of 60% determined towards affordability, 30% customer experience and 10% from coverage options.

4.6/ 5

5/5Affordability

4.4/5Customer Experience

3.3/5Coverage Points

Average Monthly Full Coverage Rate

$98Based on a 100/300/100 liability policy with $1,000 deductible comprehensive and collision coverage, per MoneyGeek's base profile methodologyAverage Monthly Minimum Coverage Rate

$43Based on a state minimum liability policy, per MoneyGeek's base profile methodologyAgent Service Rating

4.2/5Reflects aggregated ratings from independent and captive agents who represent and sell GEICO car insurance policiesUnique Coverage Option

Mechanical breakdown insurance

Amica

Best Customer Experience

MoneyGeek Rating

This score was determined with a split of 60% determined towards affordability, 30% customer experience and 10% from coverage options.

4.6/ 5

4.6/5Affordability

5/5Customer Experience

3.9/5Coverage Points

Average Monthly Full Coverage Rate

$115Based on our methodology's base profile for a 100/300/100 liability and $1,000 deductible comprehensive and collision policyAverage Monthly Minimum Coverage Rate

$57Based on our methodology's base profile for a state minimum liability coverage policyAgent Service Rating

4.7/5Aggregated from ratings for independent and captive agents representing and selling Amica car insurance policiesUnique Coverage Option

Auto-glass coverage

Progressive

Best Car Insurance Coverage Options

MoneyGeek Rating

This score was determined with a split of 60% determined towards affordability, 30% customer experience and 10% from coverage options.

4.4/ 5

4.3/5Affordability

4.5/5Customer Experience

4.9/5Coverage Points

Average Monthly Full Coverage Rate

$128Based on our methodology's base profile for a 100/300/100 liability and $1,000 deductible comprehensive and collision policyAverage Monthly Minimum Coverage Rate

$68Based on our methodology's base profile for a state minimum liability coverage policyAgent Service Rating

4.6/5Aggregated from ratings for independent and captive agents representing and selling Progressive car insurance policiesUnique Coverage Option

Custom parts and equipment

State Farm

Best Discount Programs for Young Drivers

MoneyGeek Rating

This score was determined with a split of 60% determined towards affordability, 30% customer experience and 10% from coverage options.

4.4/ 5

4.5/5Affordability

4.5/5Customer Experience

3.3/5Coverage Points

Average Monthly Full Coverage Rate

$124Based on our methodology's base profile for a 100/300/100 liability and $1,000 deductible comprehensive and collision policyAverage Monthly Minimum Coverage Rate

$53Based on our methodology's base profile for a state minimum liability coverage policyAgent Service Rating

4.5/5Aggregated from ratings for independent and captive agents representing and selling State Farm car insurance policiesUnique Coverage Option

Rideshare coverage

Best Car Insurance Companies by State

At the state level, regional carriers beat national brands on price and service more than national rankings suggest. Their business is concentrated in a smaller market, so claims and agent networks are built around local conditions rather than national averages. The table below covers regional and national carriers for each state.

| Alabama | AIG | 1 | 8 | 6 |

| Alaska | Geico | 1 | 3 | 3 |

| Arizona | Travelers | 1 | 2 | 4 |

| Arkansas | Travelers | 2 | 2 | 6 |

| California | Progressive | 2 | 3 | 2 |

| Colorado | American National | 1 | 10 | 5 |

| Connecticut | Geico | 1 | 4 | 6 |

| Delaware | Travelers | 1 | 1 | 4 |

| District of Columbia | Erie Insurance | 2 | 1 | 2 |

| Florida | Travelers | 1 | 1 | 4 |

| Georgia | Auto Owners | 2 | 1 | 7 |

| Hawaii | Geico | 1 | 4 | 5 |

| Idaho | State Farm | 1 | 4 | 6 |

| Illinois | Auto Owners | 2 | 1 | 6 |

| Indiana | Travelers | 3 | 2 | 5 |

| Iowa | Travelers | 1 | 2 | 5 |

| Kansas | Travelers | 2 | 2 | 5 |

| Kentucky | Travelers | 1 | 2 | 5 |

| Louisiana | Progressive | 5 | 1 | 2 |

| Maine | Travelers | 1 | 2 | 4 |

| Maryland | Travelers | 3 | 2 | 5 |

| Massachusetts | Plymouth Rock Insurance | 1 | 3 | 1 |

| Michigan | Travelers | 1 | 2 | 5 |

| Minnesota | Auto Owners | 2 | 1 | 5 |

| Mississippi | Travelers | 2 | 1 | 5 |

| Missouri | Auto Owners | 1 | 1 | 6 |

| Montana | State Farm | 1 | 2 | 5 |

| Nebraska | Auto Owners | 3 | 1 | 6 |

| Nevada | Travelers | 1 | 1 | 4 |

| New Hampshire | Auto Owners | 6 | 1 | 6 |

| New Jersey | Plymouth Rock Insurance | 1 | 3 | 1 |

| New Mexico | Central Insurance | 2 | 3 | 1 |

| New York | Progressive | 2 | 4 | 1 |

| North Carolina | Progressive | 2 | 2 | 2 |

| North Dakota | Auto Owners | 6 | 1 | 5 |

| Ohio | Auto Owners | 1 | 1 | 7 |

| Oklahoma | Progressive | 1 | 1 | 2 |

| Oregon | Progressive | 1 | 2 | 2 |

| Pennsylvania | Erie Insurance | 2 | 1 | 3 |

| Rhode Island | Amica | 2 | 1 | 5 |

| South Carolina | Auto Owners | 3 | 1 | 5 |

| South Dakota | Progressive | 1 | 2 | 2 |

| Tennessee | Auto Owners | 1 | 1 | 6 |

| Texas | State Farm | 1 | 3 | 6 |

| Utah | Auto Owners | 2 | 1 | 5 |

| Vermont | State Farm | 3 | 3 | 6 |

| Virginia | Travelers | 1 | 3 | 5 |

| Washington | Geico | 1 | 6 | 6 |

| West Virginia | Erie Insurance | 2 | 1 | 3 |

| Wisconsin | Travelers | 2 | 3 | 5 |

| Wyoming | State Farm | 2 | 1 | 3 |

Rates at the Best Car Insurance Companies

Rate differences at the best car insurance companies are larger than most drivers expect. The chart below shows why comparison shopping matters: across the full market, two insurers can charge nearly identical rates for one coverage level and differ by $100 or more for another. Your rate will fall above or below these averages based on your state, age, driving record and credit score.

Coverage Options at the Best Car Insurance Companies

The best car insurance company offers the coverage you need. A top rating means little if it doesn't include accident forgiveness, rideshare coverage or new car replacement for your situation. The table below shows which of our top five companies offer each coverage type, followed by an explanation of what each covers and when it's worth having.

How to Use These Rankings to Find Your Best Company

The best car insurance company for you depends on your driver profile, location and priorities. Use the steps below to narrow our rankings to your top options, then compare quotes for your actual rate.

If price is your top priority

If price is your top priorityThe same coverage from two different insurers can differ by $100 or more a month for the same driver. State matters too: regional carriers like Auto-Owners and Erie beat national brands on price in several states with almost no brand recognition outside their home markets. Get at least three quotes before deciding. Start with GEICO nationally, then check your state table to see if a regional carrier beats it where you live.

If you want the best experience when something goes wrong

If you want the best experience when something goes wrongPrice and claims satisfaction don't move together. The cheapest carriers rank lowest on claims handling, and that gap shows up after you file, not before. Start with Amica. Its claims handling and agent service scores are the highest of any national insurer we rated.

If you want the best balance of price and service

If you want the best balance of price and serviceMost drivers want a carrier that's priced well and reliable when they need it. Travelers fits that better than any other carrier we rated: it finishes second on both affordability and customer experience with no major weakness in either.

Know the coverage you need before shopping

Know the coverage you need before shoppingBefore getting quotes, figure out how much coverage you need. Then use MoneyGeek's car insurance calculator and the company comparison table to evaluate rates against the national average for your driver profile. The averages above are starting points; your rate depends on your state, driving record and credit score.

Decide if you want an agent or want to manage everything online

Decide if you want an agent or want to manage everything onlineSome of the best carriers on this page are agent-only. Travelers and State Farm don't offer online quotes or online policy management. That rules them out for many drivers, regardless of rankings. If you want a fully digital experience, GEICO and Progressive are your best options. The online-only model works best for single drivers or couples with a clean record and straightforward coverage needs. An agent is worth it when you have multiple cars, teenage drivers or a more complex financial situation.

Best Car Insurance: FAQ

What is the best car insurance company for young drivers under 25?

State Farm is the best car insurance company for young drivers under 25. The Steer Clear program and the good student discount stack together in a way no other carrier matches. Travelers is the second-best choice for this age group, with competitive rates and high service scores.

What is the best car insurance company for senior drivers over 65?

Amica is the best car insurance company for senior drivers over 65, with a 5-out-of-5 customer experience rating. Rates get more competitive relative to other carriers as drivers age. The company ranks second nationally for senior driver affordability.

Which car insurance companies offer new car replacement coverage?

Two national carriers offer new car replacement: Travelers and Liberty. Travelers provides the longest window at five years, compared to the one-to-two-year window most competitors offer.

Which car insurance companies have rideshare coverage?

Five national carriers offer rideshare coverage: Travelers, Amica, Progressive, State Farm and Allstate. This coverage pays for damage and liability costs during logged-in periods while drivers are waiting for ride requests.

Is a regional car insurance company better than a national company?

Regional insurers beat national carriers at the state level more than national rankings suggest, with lower prices and higher service scores in their home markets. Auto-Owners ranks first in 42% of states where it operates. Many regional carriers offer fewer digital tools, and the buying process can take longer.

MoneyGeek evaluated more than 70 insurance companies nationwide, including national, regional and local insurers across all U.S. residential areas. Scores reflect three weighted factors:

Affordability (60%): Quotes for multiple driver profiles across all states anchor this score, starting with a baseline 40-year-old with good credit, a clean record and no prior claims. Additional profiles for young drivers, seniors and drivers with violations produced accurate rankings across all demographics.

Customer experience (30%): Satisfaction data from Google reviews, J.D. Power ratings, AM Best financial strength scores and forum discussions informed this score. Results were broken out by state to capture geographic performance differences.

Coverage options (10%): Each provider's range of coverage types and unique policy features determined this score, with higher marks for carriers that go beyond standard liability offerings.

See our full methodology.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident insurance expert. He has spent nearly a decade analyzing the market, first at LendingTree and now at MoneyGeek, where he produces original research on hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

He covers economics and insurance at MoneyGeek, and his work has been featured in The Washington Post, The New York Times and NPR, among other outlets.

Like all MoneyGeek analysts, he draws on independent cost and consumer experience data. No insurance company partnership influences his recommendations.

Fitzpatrick earned his degrees from Johns Hopkins University (M.A. Economics and International Relations) and Boston College (B.A.). His career began in financial risk management at State Street. He's also a five-time “Jeopardy!” champion.

Sources

- AM Best. "Ratings." Accessed June 22, 2026.

- J.D. Power. "J.D. Power Auto Insurance Study." Accessed June 22, 2026.

- Progressive. "Progressive Insurance Reviews." Accessed June 22, 2026.