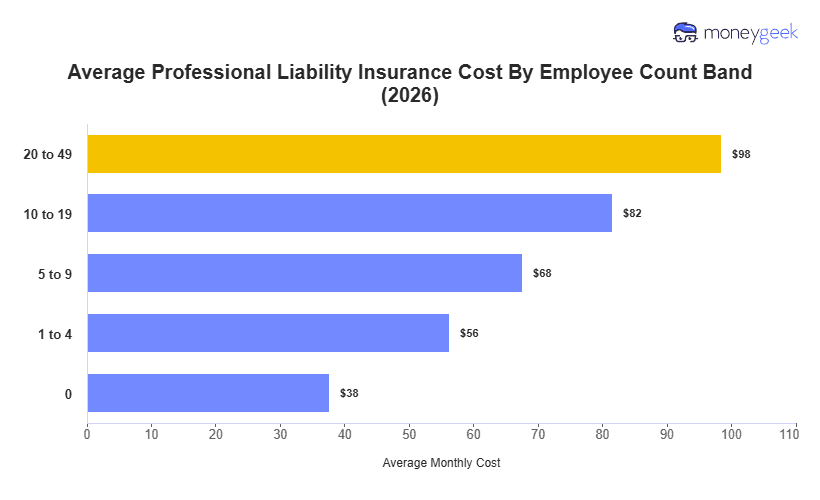

At the national level, professional liability insurance costs sit at $56/mo or $675/yr on average for a 1-to-4-person small business getting a $1 million per claim and $2 million aggregate policy.

This average price is aggregated across 151 industries and all states and territories in the United States we studied that represent most small companies that need coverage based their actual service risk. Keep in mind this national cost may not apply to you and it should be used as a starting point rather than an actual quote.

For more personalized small business insurance cost estimates, you can use our professional liability insurance calculator below.