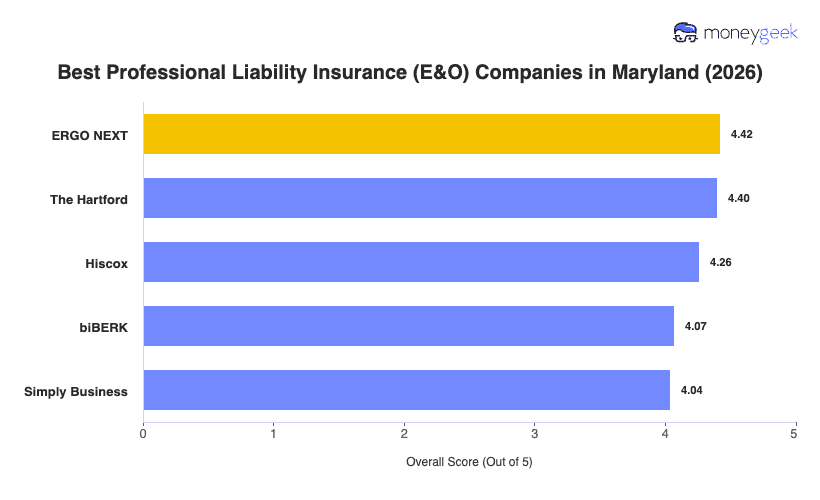

Our analysis of Maryland professional liability insurers found three providers that consistently outperformed the rest on overall score:

- ERGO NEXT holds the top overall score in Maryland, backed by the strongest customer experience rating and the best coverage score in the state. The buying process is fully digital. You get a quote, bind coverage and download your certificate without waiting for a callback or going through a broker. That matters for Maryland's large population of independent contractors and solo practitioners who need proof of coverage on short notice for a client contract. ERGO NEXT ranks first in Maryland for healthc are, fitness, pet care, real estate and other professional services. Engineers, architects and large construction operations aren't a good fit, since the insurer's underwriting skews toward smaller service businesses.

- The Hartford earns the second-place ranking for its profession-specific underwriting, which most carriers can't match. For Maryland businesses in consulting, financial services, tech, marketing and hospitality, The Hartford ranks first in the state across all of those industries, which means it prices competitively and structures coverage well for the specific claim types those professions see. The exception is health care and other professional services, where it ranks ninth in Maryland, well behind the field. Medical practices should look elsewhere.

- Hiscox covers more industries than any competitor and prices well for the ones where it leads. In Maryland, it ranks first in childcare, cleaning services, and nonprofits, and its coverage score remains strong even at lower price points. A small nonprofit in Baltimore or a childcare facility in Annapolis should pull a Hiscox quote first. Sole practitioners and firms under 10 employees across any industry will find it easier to buy here than through most traditional carriers.

These three providers suit most Maryland businesses well, but no ranking replaces side-by-side comparison. Comparing business insurance options across carriers before you buy gives you the clearest read on price and fit.