Financial services businesses need business insurance because the work itself creates consistent exposure: the advice you give, the client financial data you store, the errors that can surface months after a filing or report is complete, and the staff you employ to do it.

Those exposures include:

- A tax preparer's filing error that triggers IRS penalties a client holds you responsible for

- A bookkeeper's reconciliation mistake that causes a small business client to misstate financials to their lender

- A data breach exposing the Social Security numbers, bank account details and income records of every client in your system

- A financial advisor's investment recommendation that a client claims was unsuitable for their risk tolerance

- A payroll processor's withholding error that generates IRS notices across multiple client accounts simultaneously

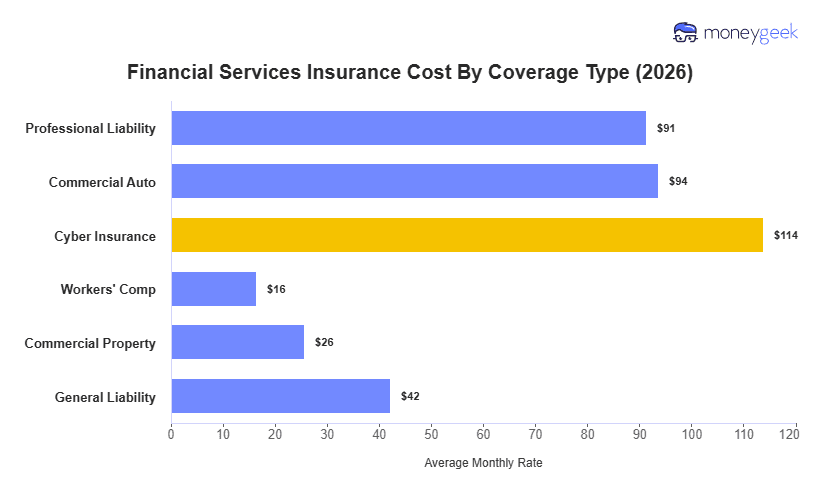

What we've found is that most financial services businesses are more exposed on professional liability and cyber than on general liability. A bookkeeping error from eight months ago or a data breach no one noticed for weeks can generate a claim long after the work was done and the client moved on.

If you want guidance specific to your type of financial services practice, the resources below break it down by business model.