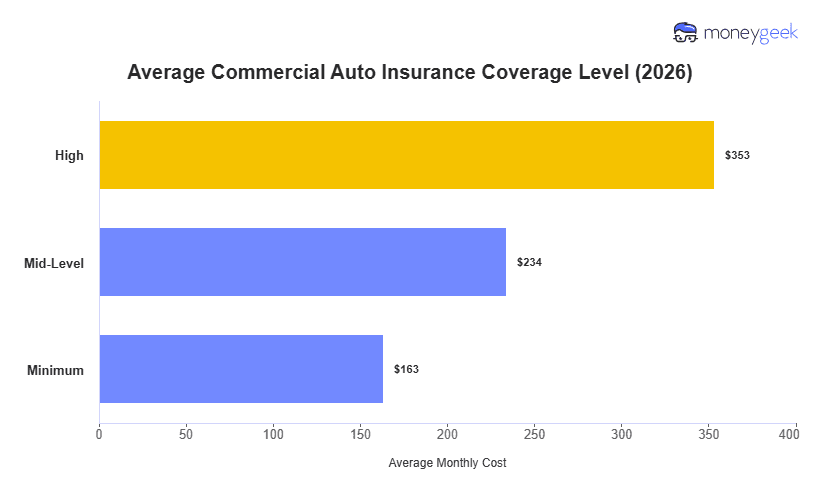

Commercial auto insurance costs $163 per month ($1,959 per year) for minimum coverage. This is a national benchmark derived from eight vehicle types across 25 general industry categories (including 400+ sub-industries) and all 50 states (including D.C.) to reflect the range of commercial fleet profiles.

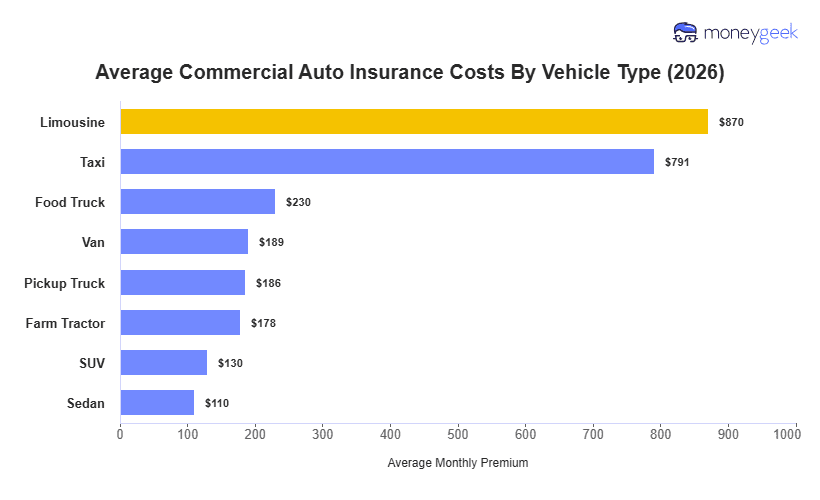

However, your small business insurance rates will vary heavily depending on your vehicle's details, your drivers, and details surrounding your business's operations and location. This also does not represent commercial truck insurance costs, which we consider a completely separate category inclusive of larger cargo and livery vehicles like box trucks, semis, tankers and dump trucks.