New York businesses pay $211 per month ($2,537 per year) for minimum coverage commercial auto insurance, based on MoneyGeek's analysis of eight vehicle types across 25 general industry categories. That puts New York well above the national average of $163 per month and above every neighboring state in the region.

New Jersey comes closest at $209 per month, followed by Massachusetts ($202), Rhode Island ($201) and Connecticut ($193). Pennsylvania and Vermont sit well below the rest, at $79 and $92 per month respectively.

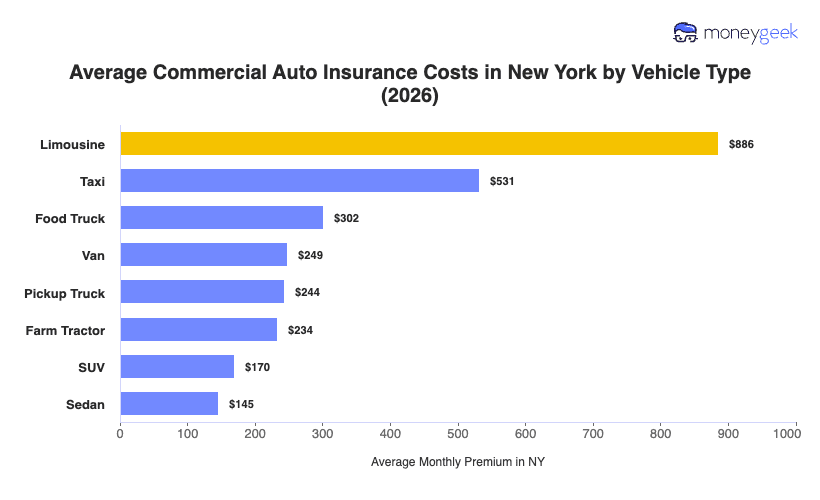

Commercial auto insurance rates in New York are driven by the state's dense urban traffic, high litigation rates and some of the heaviest claim costs in the country. Your average commercial auto insurance cost will differ from that state benchmark depending on your vehicle, your drivers and what your business does.