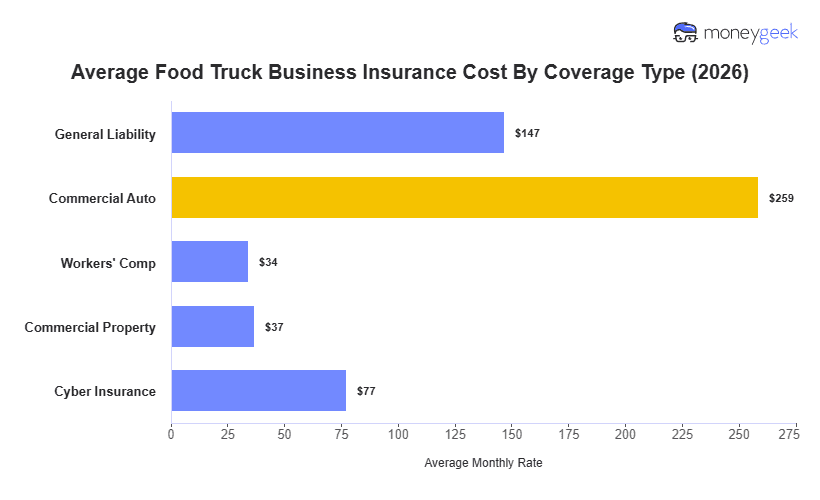

Food truck insurance costs about $443 per month for a recommended startup package with commercial auto, general liability and commercial property insurance. A minimum requirements package with only commercial auto and general liability costs about $406 per month, while a broader package with cyber insurance added costs about $520 per month. If you're adding employees, factor in $34/mo per employee and $259/mo per food truck you add to your fleet.

Keep in mind these are modeled benchmark averages (not quotes) for a 1–4-employee operation across all 50 states, and the bundle costs presented are before discounts are applied. Your actual premium will vary based on factors such as your state, employee count, and claims history, but these figures provide a realistic range to evaluate quotes against.

Below, you can compare insurance bundle costs and the coverages they include for food trucks.