Food and beverage insurance costs range widely because a vending machine service and a full-service catering company carry very different risk profiles. The average cost of business insurance for food and beverage businesses is $101 monthly, or $1,209 annually. Those figures reflect 26 subindustries across 50 states and Washington, D.C. The analysis used quotes from the five most common coverage types for businesses with one to four employees, and the numbers are best read as benchmarks rather than quotes.

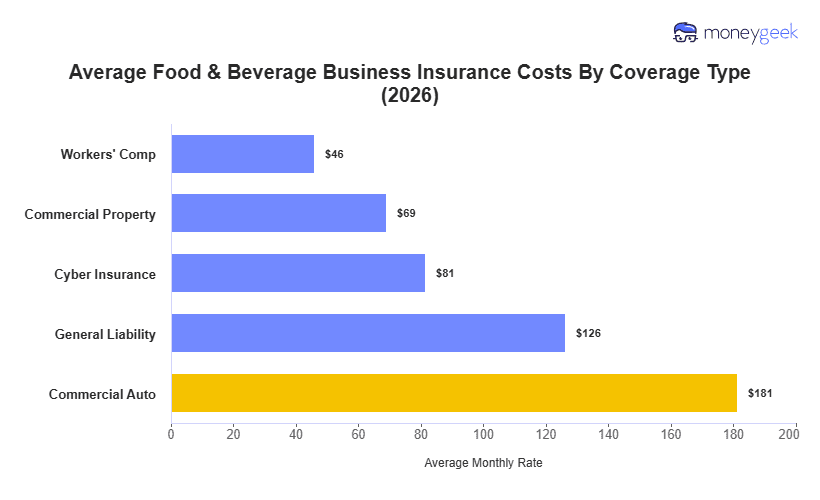

The spread across coverage types runs from $46 monthly for workers' comp to $181 monthly for commercial auto. Workers' comp prices on payroll, which keeps those rates low for small kitchen and counter crews. Commercial auto lands highest because vehicle use in this industry is intensive. Food trucks run daily service, caterers haul equipment to events and pizza or meal delivery puts drivers on the road repeatedly. The breakdowns below show how costs shift by coverage type: