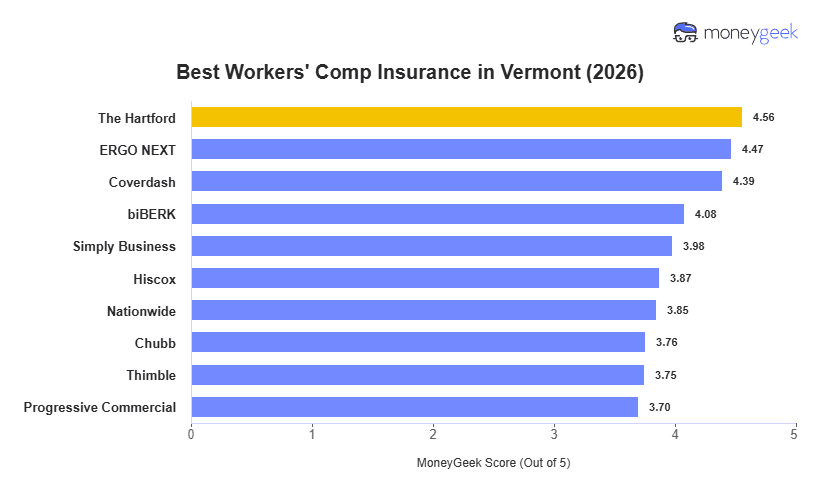

The Hartford tops our analysis for the best workers' comp insurance in Vermont, delivering competitive rates, outstanding customer support and comprehensive coverage options. ERGO NEXT and Coverdash round out the top three, both providing reliable alternatives for Vermont business owners.

Best Workers' Comp Insurance in Vermont (2026)

With rates as low as $9 per month, The Hartford, ERGO NEXT and Coverdash offer the best workers' comp insurance in Vermont.

Get matched to top Vermont workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 30, 2026

Advertising & Editorial Disclosure

Best Vermont Workers' Comp Insurance: Fast Answers

What are the best and cheapest workers' comp insurance providers in Vermont?

The Hartford is Vermont's cheapest workers' comp provider at $82 a month and is also the best workers' comp insurance option in the state, based on our analysis of affordability, customer experience and coverage options. The five most affordable providers are:

- The Hartford: $82 a month

- ERGO NEXT: $83 a month

- Coverdash: $96 a month

- biBERK: $102 a month

- Thimble: $109 a month

Is workers' comp insurance required in Vermont?

Vermont mandates workers' compensation insurance for most employers with employees. Key exemptions include sole proprietors without employees, domestic workers in private homes working under 40 hours weekly and certain agricultural operations. Non-compliance results in fines up to $5,000 plus potential criminal charges and civil liability for workplace injuries.

How much does workers' comp insurance cost in Vermont?

Workers' compensation insurance costs in Vermont average $107 per employee monthly for a two-person business. Rates vary based on your industry and payroll size, from $15 per month for Beauty, Body & Wellness Services businesses to $322 for Transportation & Logistics businesses.

How do you get workers' comp insurance in Vermont?

Vermont is a private competitive market with no state fund, so employers get workers' compensation insurance directly from licensed private carriers. Employers who can't secure coverage in the voluntary market may access the assigned risk pool as a fallback option.

What does Vermont workers' comp insurance cover?

Workers' compensation in Vermont covers:

- Medical expenses for work-related injuries, from minor cuts at a Montpelier office to serious accidents at Burlington construction sites

- Wage replacement benefits during recovery periods when employees cannot work

- Disability payments for permanent impairments that affect future earning capacity

- Survivor benefits for families of workers who die from job-related incidents

Best Workers' Comp Insurance Companies in Vermont

| The Hartford | 4.56 | $82 | 3 | 3 |

| ERGO NEXT | 4.47 | $83 | 1 | 6 |

| Coverdash | 4.39 | $96 | 5 | 1 |

| biBERK | 4.08 | $102 | 8 | 8 |

| Simply Business | 3.98 | $114 | 2 | 2 |

| Hiscox | 3.87 | $113 | 6 | 10 |

| Nationwide | 3.85 | $113 | 6 | 5 |

| Chubb | 3.76 | $134 | 3 | 4 |

| Thimble | 3.75 | $109 | 8 | 9 |

| Progressive Commercial | 3.70 | $118 | 8 | 7 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

The Hartford

Best Workers' Comp Insurance in Vermont

MoneyGeek Rating

4.6/ 5

4.9/5Affordability Score

4.1/5Customer Experience Score

4/5Coverage Score

Average Monthly Cost

$82Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

ERGO NEXT

Best Vermont Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.5/ 5

4.8/5Affordability Score

4/5Customer Experience Score

3.8/5Coverage Score

Average Monthly Cost

$83Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

LEARN MORE ABOUT VERMONT BUSINESS INSURANCE

Cheapest Workers' Comp Insurance Companies in Vermont

The Hartford has the cheapest workers’ compensation insurance in Vermont at $82 monthly per employee ($984 annually). ERGO NEXT follows closely at $83 monthly, while Coverdash ranks third at $96.

The pricing difference between providers can have a major affect on long-term costs for small businesses in our analysis. For example, the gap between The Hartford ($82) and Thimble ($109) equals roughly $324 more annually per employee. Businesses with multiple employees and lower-risk operations benefit most from these savings, while pricing differences narrow in higher-risk industries where underwriting plays a larger role in final premiums.

| The Hartford | $82 | $984 |

| ERGO NEXT | $83 | $996 |

| Coverdash | $96 | $1,152 |

| biBERK | $102 | $1,224 |

| Thimble | $109 | $1,308 |

| Hiscox | $113 | $1,356 |

| Nationwide | $113 | $1,356 |

| Simply Business | $114 | $1,368 |

| Progressive Commercial | $118 | $1,416 |

| Chubb | $134 | $1,608 |

Cheapest Workers' Comp in Vermont by Industry

The Hartford has the lowest workers’ compensation rates in more Vermont industries than any other provider in our analysis, ranking cheapest in 12 of the 25 industries we reviwed. Its strongest pricing appears in lower-risk, office-based industries.

ERGO NEXT is the more affordable option for most Vermont businesses in physically demanding or higher-risk industries, including construction and contracting ($202 a month), transportation and logistics ($253 a month) and agriculture and natural resources ($138 a month). Coverdash has the lowest rates in two industries, including childcare services ($30 a month) and fitness services ($55 a month).

| Financial Services | The Hartford | $9 | $108 |

| Beauty, Body & Wellness Services | ERGO NEXT | $11 | $132 |

| Marketing & Communications | The Hartford | $12 | $144 |

| Consulting Services | The Hartford | $14 | $168 |

| Real Estate & Property Services | The Hartford | $14 | $168 |

| Other Professional Services | The Hartford | $17 | $204 |

| Tech/IT | The Hartford | $28 | $336 |

| Childcare Services | Coverdash | $30 | $360 |

| Hospitality, Travel & Tourism | The Hartford | $32 | $384 |

| Healthcare & Medical | The Hartford | $34 | $408 |

| Food & Beverage | ERGO NEXT | $35 | $420 |

| Retail & Product Rental | The Hartford | $38 | $456 |

| Nonprofit & Associations | The Hartford | $44 | $528 |

| Pet Care Services | ERGO NEXT | $54 | $648 |

| Fitness Services | Coverdash | $55 | $660 |

| Education | ERGO NEXT | $57 | $684 |

| Repair & Maintenance | ERGO NEXT | $62 | $744 |

| Arts, Media & Entertainment | ERGO NEXT | $80 | $960 |

| Cleaning Services | The Hartford | $92 | $1,104 |

| Recreation & Sports | ERGO NEXT | $94 | $1,128 |

| Manufacturing | The Hartford | $112 | $1,344 |

| Agriculture & Natural Resources | ERGO NEXT | $138 | $1,656 |

| Wholesale & Distribution | ERGO NEXT | $161 | $1,932 |

| Construction & Contracting | ERGO NEXT | $202 | $2,424 |

| Transportation & Logistics | ERGO NEXT | $253 | $3,036 |

How Much Is Workers' Comp Insurance in Vermont?

Our analysis of Vermont workers’ compensation rates shows that industry classification has a much bigger impact on pricing than many businesses expect. Vermont businesses pay about $107 monthly per employee on average, roughly 45% above the national average of $74, but actual costs range from $15 monthly for beauty and wellness businesses to $322 for transportation companies.

For most employers, statewide averages provide limited insight into real insurance costs. A consulting firm may pay around $22 monthly per employee, while a trucking company can pay more than $300 for the same required coverage. Industry risk classification is the primary factor driving workers’ compensation premiums in Vermont.

| Beauty, Body & Wellness Services | $15 | $180 |

| Financial Services | $16 | $192 |

| Marketing & Communications | $17 | $204 |

| Consulting Services | $22 | $264 |

| Real Estate & Property Services | $23 | $276 |

| Other Professional Services | $25 | $300 |

| Childcare Services | $39 | $468 |

| Food & Beverage | $43 | $516 |

| Tech/IT | $45 | $540 |

| Hospitality, Travel & Tourism | $46 | $552 |

| Healthcare & Medical | $54 | $648 |

| Retail & Product Rental | $58 | $696 |

| Nonprofit & Associations | $61 | $732 |

| Pet Care Services | $67 | $804 |

| Fitness Services | $69 | $828 |

| Education | $70 | $840 |

| Repair & Maintenance | $78 | $936 |

| Arts, Media & Entertainment | $98 | $1,176 |

| Recreation & Sports | $122 | $1,464 |

| Cleaning Services | $127 | $1,524 |

| Manufacturing | $151 | $1,812 |

| Agriculture & Natural Resources | $174 | $2,088 |

| Wholesale & Distribution | $194 | $2,328 |

| Construction & Contracting | $297 | $3,564 |

| Transportation & Logistics | $322 | $3,864 |

Vermont Workers' Comp Insurance Cost Factors

Vermont workers' comp rates are set under the NCCI class code system and regulated by the Vermont Department of Financial Regulation. The state's private competitive market structure, combined with above-average benefit levels, is the primary driver of Vermont's cost position above the national average of $74 a month.

How Much Workers' Comp Insurance Do I Need in Vermont?

Vermont law mandates workers' compensation coverage for all employers with one or more employees, including part-time workers. You don't select coverage amounts since Vermont sets statutory benefits your policy must provide: unlimited medical coverage, two-thirds of average weekly wages for temporary disability, and permanent disability benefits based on injury severity.

Coverage costs are based on your payroll and industry classification code, not a limit you choose. Penalties for noncompliance include up to $100 daily for the first seven days without coverage, $150 daily thereafter, and potential stop-work orders shutting down your business.

Vermont Workers' Comp Insurance Exemptions

You're required to have coverage in Vermont, but some business categories are exempt from workers' comp requirements:

- Agricultural/Farm Employers with Less Than $10,000 Annual Payroll: Vermont exempts farm employers whose aggregate payroll is less than $10,000 in a calendar year from carrying workers' comp insurance.

- Corporate Officers and LLC Members (With Approval): Corporate officers and LLC members are automatically covered in Vermont, but may elect exclusion with prior approval from the Vermont Department of Labor.

- Independent Contractors Meeting Vermont Criteria: An independent contractor who meets Vermont's specific criteria under 21 V.S.A. § 601(14)(F) is exempt when they have a written agreement, work independently with no employees, and haven't contracted with other independent contractors.

- Sole Proprietors and Partners: A sole proprietor or partner in an unincorporated business is automatically excluded from Vermont workers' comp coverage but may elect to be covered.

- Self-Employed Individuals: Self-employed business owners in Vermont are not required to carry workers' comp insurance for themselves, but can voluntarily purchase coverage.

- Casual Workers: Workers performing casual services in or about a private dwelling that are not part of the employer's usual Vermont business operations are exempt from coverage.

- Domestic Service Workers: Individuals employed in domestic service in or about a private home in Vermont are exempt from workers' comp requirements.

- Family Members: Family members of Vermont employers who reside in the employer's household are exempt from mandatory workers' comp coverage.

- Real Estate Professionals: Licensed real estate brokers and salespersons in Vermont who meet independent contractor criteria are exempt from workers' comp coverage requirements.

- Agricultural/Farm Workers (Small Farms): Workers employed by Vermont agricultural employers with less than $10,000 annual aggregate payroll are exempt from workers' comp coverage.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal workers' comp programs supersede Vermont's state requirements for certain employee categories. The Federal Employees' Compensation Act (FECA) covers federal civilian employees. The Federal Employers' Liability Act (FELA) applies to railroad workers. The Longshore and Harbor Workers' Compensation Act covers maritime employees. Vermont employers with workers in any of these categories should confirm which federal program governs their coverage obligations before purchasing a state policy.

How to Get the Best Workers' Comp Insurance in Vermont

Follow these steps to secure the right workers' comp coverage for your Vermont business.

- 1Confirm Vermont Coverage Requirements

Check your coverage obligations with the Vermont Department of Financial Regulation. Requirements depend on employee count, business structure and whether any exemptions apply to your workforce. Confirm current thresholds and penalties for non-compliance directly with the state agency.

- 2Identify Your NCCI Class Codes Accurately

The state of Vermont uses NCCI class codes to assign base rates by job duty. Pull the correct codes for every employee role in your business before requesting quotes. Incorrect class code assignments can result in audit-driven premium increases at year-end.

- 3Document Payroll, Employee Count, and Claims History

Carriers price workers' comp policies based on total payroll, number of employees and your experience modification rate (EMR). Collect at least three years of payroll records and a complete claims history before approaching carriers. Accurate documentation reduces the risk of mid-term adjustments.

- 4Request Quotes From Multiple Licensed Vermont Carriers

Vermont's private competitive market means rates vary across carriers. The $27 a month spread between The Hartford at $82 a month and Thimble at $109 a month shows why comparing multiple quotes matters. Contact at least three licensed carriers or work with an independent agent who has access to multiple Vermont-admitted insurers to get a representative range of pricing.

- 5Compare Total Value, Not Just Monthly Rate

Monthly premium is important, but claims handling speed, policy management tools and audit support also affect your total cost of coverage. Review each carrier's claims processing score and policy management score alongside its rate.

- 6Complete Purchase and Establish Payroll and Audit Reporting

Bind coverage before your required effective date and set up payroll reporting procedures. Vermont workers' comp policies are audited annually, and accurate payroll reporting throughout the policy year reduces the likelihood of a large audit adjustment at renewal. Confirm your carrier's reporting format and schedule at the time of purchase.

- 7Review at Annual Renewal

Vermont workers' comp rates and your EMR can change at each renewal. Review your class codes, payroll figures, and claims history before your renewal date and request updated quotes from at least two additional carriers. A clean policy year or a reduction in your EMR may qualify you for lower rates from carriers that were previously uncompetitive.

Bottom Line

The Hartford, ERGO NEXT and Coverdash are Vermont's top workers' comp options. Research each company's service quality, maximize discounts and select coverage that fits your budget. The best choice balances monthly rate, claims support quality and alignment with your business's NCCI class codes.

Next Steps

Use these resources to move forward with Vermont workers' comp coverage. Rates vary by NCCI class code, so getting a personalized estimate is the most reliable way to confirm your actual premium.

Vermont Workers' Compensation Insurance FAQs

Does Vermont workers' comp cover employees who work remotely in other states?

Vermont workers' comp policies generally cover employees based in Vermont, but coverage for remote workers in other states depends on your policy's other-states endorsement. Employers with employees working full-time in another state may need to add that state to their policy or purchase a separate policy there. Confirm your coverage territory with your carrier before allowing employees to work remotely across state lines.

How does my experience modification rate affect my Vermont workers' comp premium?

Your experience modification rate (EMR) compares your actual claims history to the expected claims for your industry. An EMR above 1.0 increases your premium; an EMR below 1.0 reduces it. Vermont employers with three or more years of claims data will have an EMR calculated by NCCI, and that figure is applied directly to your base rate at renewal.

Can business owners opt out of workers' comp coverage in Vermont?

Sole proprietors and certain corporate officers in Vermont can exclude themselves from coverage under specific conditions. The opt-out process requires written notification to the insurer and, in some cases, to the Vermont Department of Financial Regulation. Owners who opt out remain personally responsible for any work-related injury costs not covered by a policy.

What's the difference between workers' comp and employer's liability?

Workers' comp covers your employees' medical costs and lost wages after a work-related injury without considering fault. Employer's liability, which is Part Two of a standard workers' comp policy, covers your legal costs if an injured employee sues you directly.

How long does a workers' comp claim stay on my Vermont premium record?

In Vermont, claims affect your EMR for three policy years, excluding the most recent year. A single large claim can shift your EMR above 1.0 and increase your premium for multiple renewal cycles.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Vermont using small business profiles with one to four employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. MoneyGeek then uses a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.

Sources

- Vermont Department of Labor. "Administration Fund Quarterly Assessment Instructions and Report Forms." Accessed June 30, 2026.

- Vermont Legislature. "Bill Status S.117 (Act 40)." Accessed June 30, 2026.

- Vermont Legislature. "Section 687. Security for compensation." Accessed June 30, 2026.

- PIA Northeast News. "VT: NCCI 2025 WC Loss Cost Decrease Approved." Accessed June 30, 2026.

- Vermont Department of Financial Regulation. "Workers' Compensation." Accessed June 30, 2026.