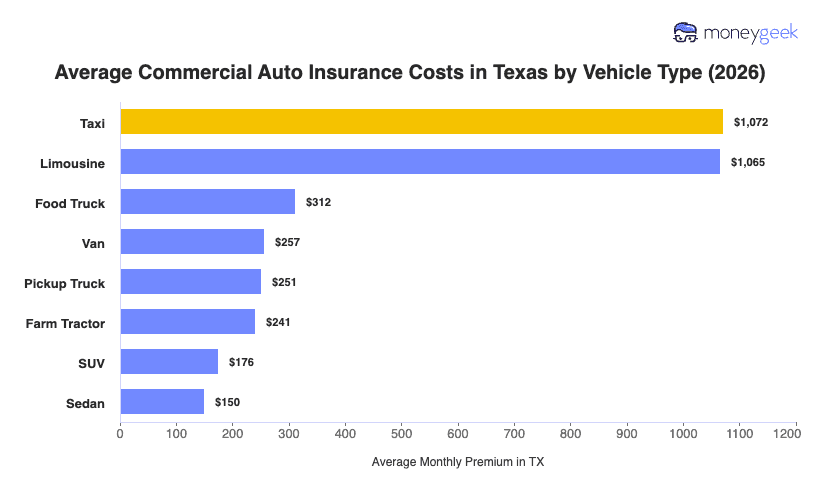

The average commercial auto insurance cost for Texas businesses is $220 per month ($2,644 per year) for minimum coverage, based on MoneyGeek's analysis of eight vehicle types across 25 general industry categories.

Texas sits well above the national benchmark of $163 per month and higher than every neighboring state in the region. Colorado comes closest to the national average among Texas neighbors at $167 per month. Arkansas ($146), Oklahoma ($145) and Louisiana ($179) all sit within $20 of the benchmark, while New Mexico ($130) runs furthest below it.

Commercial auto insurance rates in Texas are driven by the state's high population density, above-average litigation activity and elevated claim costs relative to the national market. Your commercial auto insurance rates will differ from that state benchmark depending on your vehicle, your drivers and what your business does.