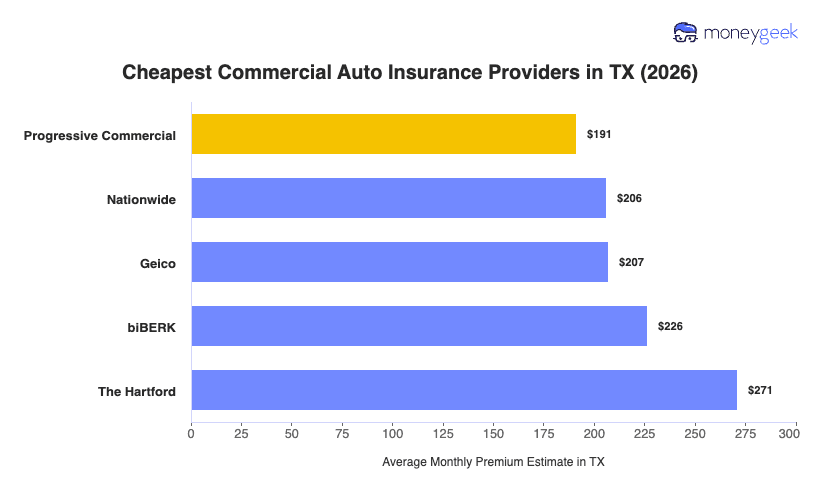

Texas businesses can compare cheapest commercial auto insurers below, with all three top-ranked providers pricing under the state average of $220 per month.

- Progressive Commercial averages $191 per month in Texas, 13% below the state average. MoneyGeek's Texas analysis shows it ranks first for affordability in 15 of 25 general industry categories, with manufacturing, wholesale and distribution, and transportation and logistics seeing the deepest savings at 26% to 28% below their respective industry averages.

- GEICO averages $207 per month in Texas, 6% below the state average. It prices most competitively for financial services businesses at 21% below the industry average and for pet care operations. Texas businesses operating sedans, SUVs, pickup trucks or farm tractors will also find GEICO ranks first on vehicle type affordability in MoneyGeek's data.

- Nationwide averages $206 per month in Texas, 7% below the state average. It doesn't rank first for any general industry category in MoneyGeek's Texas analysis, making it the better fallback for businesses whose fleet and industry profile don't align with Progressive Commercial's or GEICO's strongest segments.

Texas commercial auto insurance costs vary by fleet composition, driver records, services offered and where in Texas your business operates. Treat these rankings as a comparison starting point, not a guaranteed rate for your business.