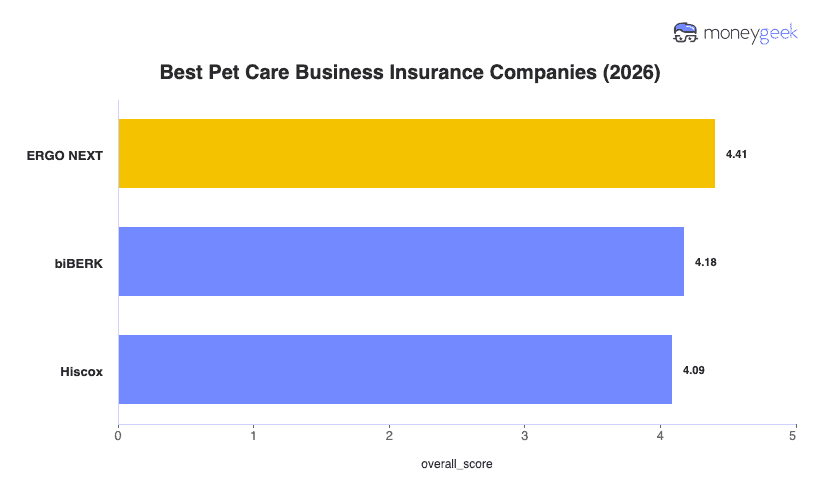

I determined the best business insurance companies for pet care services by analyzing quotes for policies that address common risks, including pets becoming injured or ill while in your care, bites and scratches, missed or late visits and contagious illnesses. Beyond cost, I looked at how quickly providers issue proof of insurance, since clients or facilities may require it before hiring you. I also considered how easy it is to get support because claims involving an injured, missing or seriously ill pet can be sensitive and complicated.

I narrowed my recommendations to these three insurers: