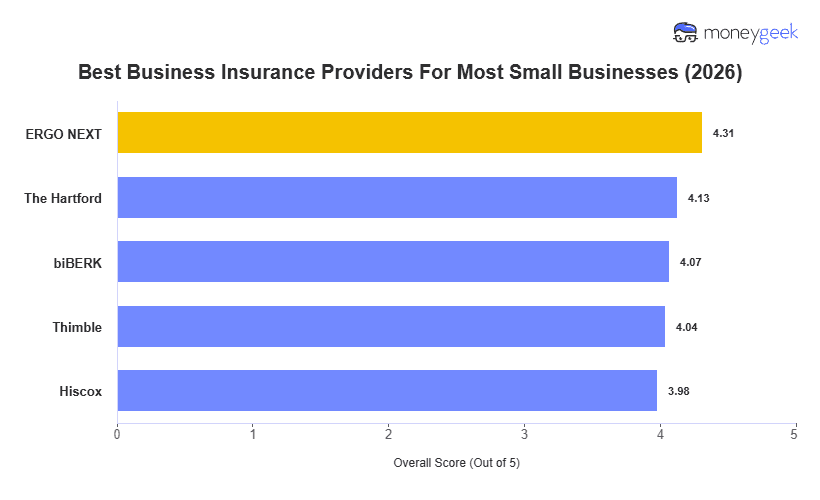

ERGO NEXT leads as the best small business insurer overall, but the right provider depends on three things specific to your situation: what your work exposes you to, how much you can spend without cutting corners on protection, and how much support you need when something goes wrong. Those factors play out differently for every company and the type of work you do, where you live and how large of an operation you have all come into play when determining who is ideal.

Each of the providers below earned a spot on my top five small business insurers for a specific grouping of company profiles:

- ERGO NEXT: Best Overall, Best For Hands-on Work Industries

- The Hartford: Best For White Collar and Larger Businesses

- biBERK: Best For Simple, Niche Businesses

- Thimble: Best For Gig and High-Risk Work

- Hiscox: Best For Tailored Professional Liability Coverage

You can also see an overview of how they ranked overall in my analysis in the summary table below for a more side-by-side view of my overall findings to ground your initial comparison.