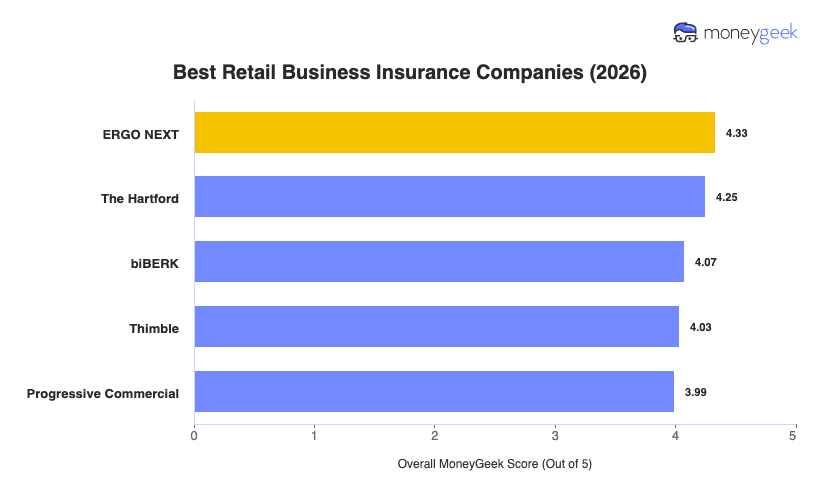

No single carrier is the best business insurance fit for every retail business. A clothing boutique dealing with slip-and-fall claims on a busy sales floor and a hardware store managing product liability exposure from items sold both need providers that understand retail risk, price inventory-heavy accounts competitively and can process a claim without forcing the storefront to go dark during peak season. These five providers consistently topped our analysis:

- ERGO NEXT: Best Overall, Best Buying Experience

- The Hartford: Best for Coverage

- biBERK: Best Direct-to-Retailer Option

- Thimble: Best for Pop-Up and Seasonal Retailers

- Progressive Commercial: Best for Retailers with Vehicles

All five earned high marks across the three areas retail owners weigh most heavily: pricing that stays predictable through renewals even as inventory values shift seasonally, coverage options that address the full retail risk profile from product liability to commercial property and responsive claims handling when a storefront loss or merchandise theft puts operations on hold. The table below breaks down what sets each one apart for retailers.