Retail businesses typically pay $129 monthly, or $1,549 annually, across the five most common coverage types. That figure comes from MoneyGeek's analysis of quotes for businesses with one to four employees across 39 retail sub-industries, four vehicle types, all 50 states and Washington, D.C., with standardized limits.

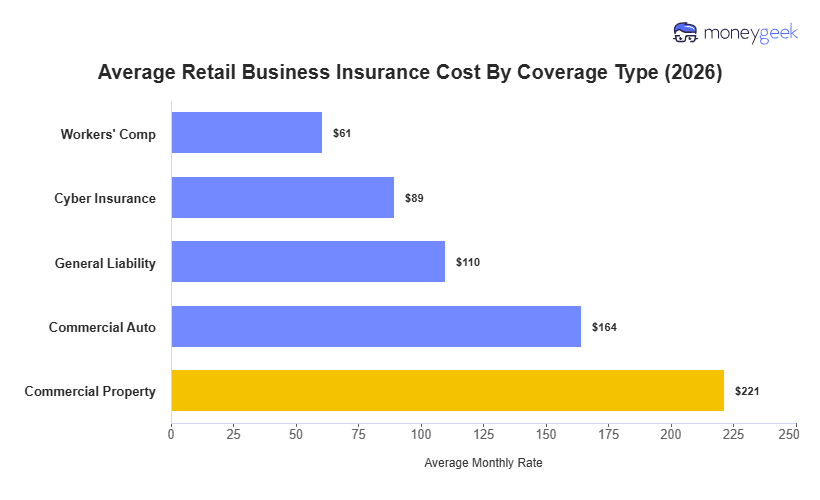

The average cost of business insurance varies by coverage type, running from $61 monthly per employee for workers' comp to $221 monthly for commercial property. Workers' comp tends to run low for retail because cashiering, stocking shelves and running a register carry lower injury exposure than physical trades, which keeps base rates modest for most store types. Commercial property is the most expensive because insurers price the inventory, fixtures and equipment inside the store. For auto parts shops, electronics retailers and stores carrying high-value stock, that exposure adds up quickly.

The table below shows average monthly and annual costs for each coverage type. These are estimates, not quotes as your actual premium will vary based on your store type, location and payroll.