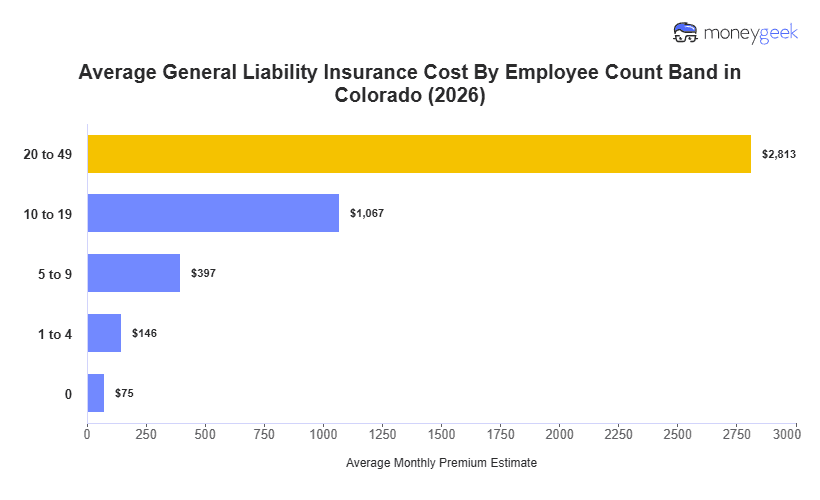

General liability insurance costs in Colorado average $146 monthly ($1,755 annually) for businesses with one to four employees and limits of $1 million per occurrence/$2 million aggregate. This figure sits 19% above the national average of $123 monthly, ranking Colorado 41st nationally for affordability.

Colorado's costs exceed both neighboring and regional benchmarks. Adjacent states like Kansas, Wyoming and Utah fall 25% to 30% below Colorado. The same pattern exists across the broader Mountain West region: Montana and Idaho businesses pay around $95 to $97 monthly. Nevada, while having higher costs at $131, is still more affordable than Colorado.

This state average serves as a reference point, not a quote. Actual costs shift based on your industry's claim exposure, specific business operations and claims history, even when coverage limits remain the same. To get a cost estimate based on your business profile, use the Colorado general liability insurance cost calculator below.