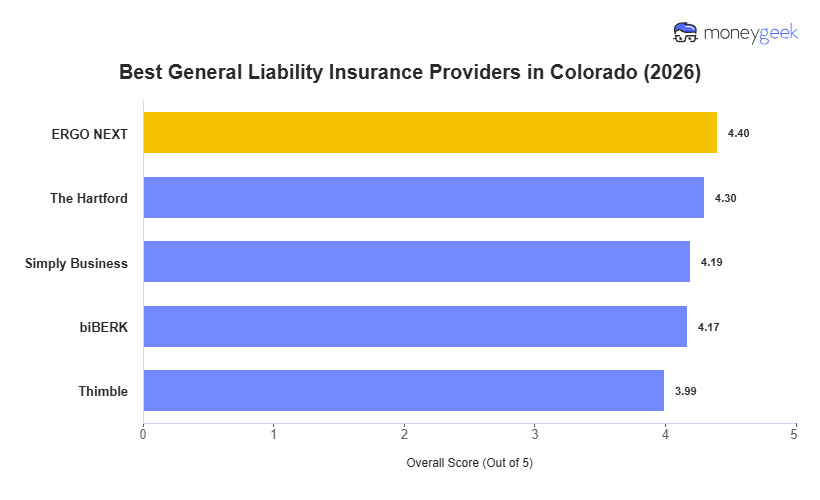

Small businesses in Colorado have liability risks shaped by the state's mix of seasonal tourism, construction growth and service-based industries. The best general liability insurance depends on what you do, how many people you employ and where in the state you operate. These five providers earned top marks for balancing affordable rates with strong service and flexible coverage:

- ERGO NEXT: Best Overall, Best for High-Risk Industries

- The Hartford: Best for Professional Services

- Simply Business: Best for Comparing Multiple Carriers

- biBerk: Best for Solopreneurs

- Thimble: Best for Gig Workers and Seasonal Businesses

These insurers address practical needs of Colorado's small business owners, whether you're running a landscaping crew in Boulder, managing a café in Colorado Springs, or operating a contracting business in the Front Range. The differences among the providers are: