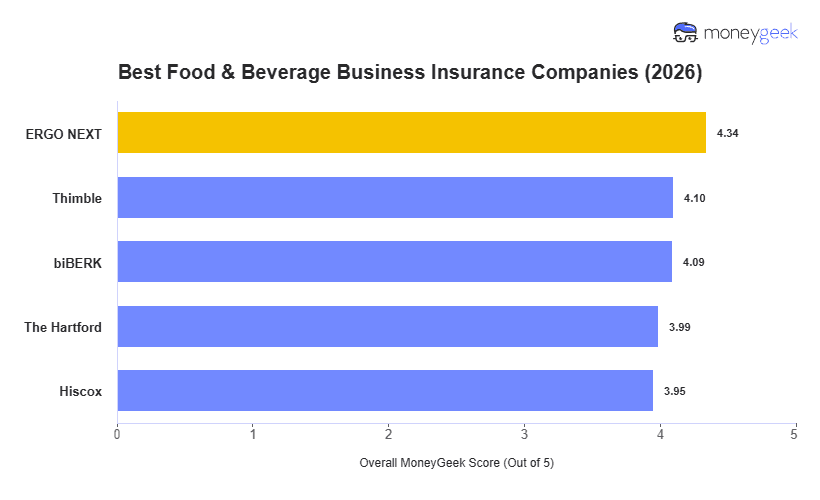

What works for a coffee shop rarely works for a banquet hall, and no single provider is the best fit for every food and beverage business. Our analysis of the best business insurance options across 26 food and beverage subindustries identified five providers that hold up well on price, service and coverage for food and beverage businesses:

- ERGO NEXT: Best Overall, Best for On-the-Go Food Operators

- Thimble: Best for Short-Term and Event-Based Food Coverage

- biBERK: Best for Owner-Operated Food Businesses

- The Hartford: Best for Coverage Options

- Hiscox: Best for Food Businesses in the Northeastern Region

All five earned high scores by balancing what food and beverage businesses actually need: pricing that stays competitive as payroll and headcount grow, a service experience that doesn't slow operations during busy seasons or after a claim, and coverage options broad enough for businesses that sell, serve or handle food. The table below shows individual scores, ranks and overall pricing for our top picks.