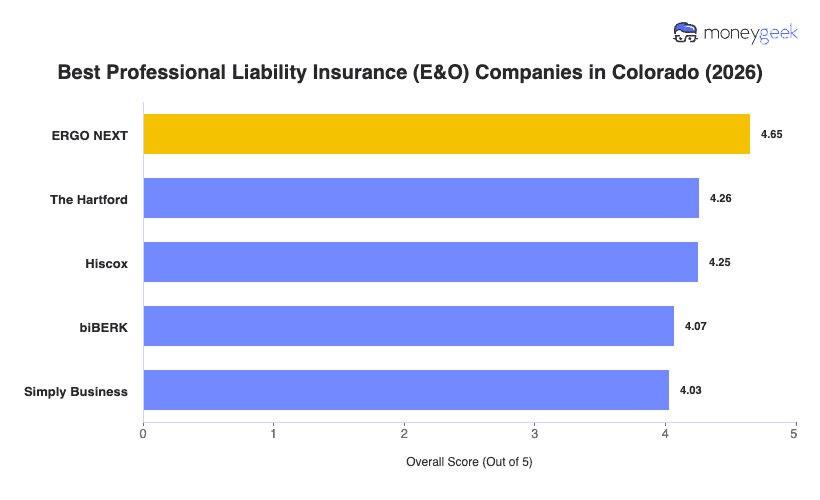

Our analysis of Colorado professional liability insurers found three providers that consistently outperformed the rest of the field on rates, coverage quality and customer experience.

- ERGO NEXT: It earns the top spot by pairing the state's lowest rates with a genuinely fast buying experience. Denver consultants and Boulder tech startups can get quoted, buy a policy and pull a certificate of insurance in about 10 minutes through the app or website, with 24/7 policy management after that. Businesses in consulting, finance, education and tech score better with competing providers, so those industries should weigh their options before committing.

- The Hartford: For Colorado businesses that expect to actually use their coverage, claims handling matters more than shaving a few dollars off the monthly rate, and this is where The Hartford earns its spot. Backed by more than 200 years in the industry, it ranks first or second in Colorado for Hospitality, Travel and Tourism, Marketing and Communications, and Education. Health care professionals and other professional services businesses should look elsewhere. The Hartford underperforms in both categories in this state.

- Hiscox: Coverage breadth is what sets Hiscox apart. It writes professional liability across more than 180 industries and ranks second in Colorado for Financial Services, Consulting, Tech/IT and Childcare. Businesses in Arts, Media and Entertainment or Recreation and Sports will find better fits elsewhere on this list.

These three providers cover the needs of most Colorado businesses well, but no ranking captures every variable your business brings to the table. Comparing business insurance options side by side and getting direct quotes gives you the clearest picture of what you'll actually pay and what you'll actually get.