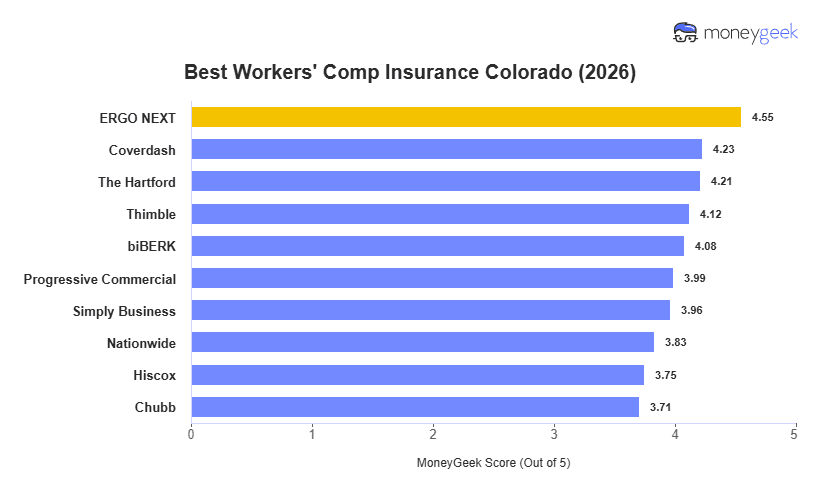

One pattern was evident in our Colorado workers' comp analysis: the carriers with the strongest coverage rankings don't always have the lowest rates. Coverdash ranks first for coverage at $109 per month, while ERGO NEXT leads on price at $78 per month but ranks sixth for coverage. For most Colorado small businesses with fewer than five employees, that trade-off is the core decision. Whether rate savings or coverage depth matters more depends on your industry's injury risk profile.

The spread between the cheapest provider, ERGO NEXT, and the most expensive, Chubb, is $69. Low-hazard Colorado employers in professional services, tech, and consulting gain the most from that gap. That advantage shrinks in construction and transportation. ERGO NEXT's construction rate of $184 still beats the $314 state average, but the dollar gap between carriers is smaller.