A telecom provider negotiating a major contract and a two-person web design studio shopping their first policy both want the best business insurance, but they might not find it from the same carrier. Our analysis of major business insurance providers identified five that consistently perform well across the range of tech operations.

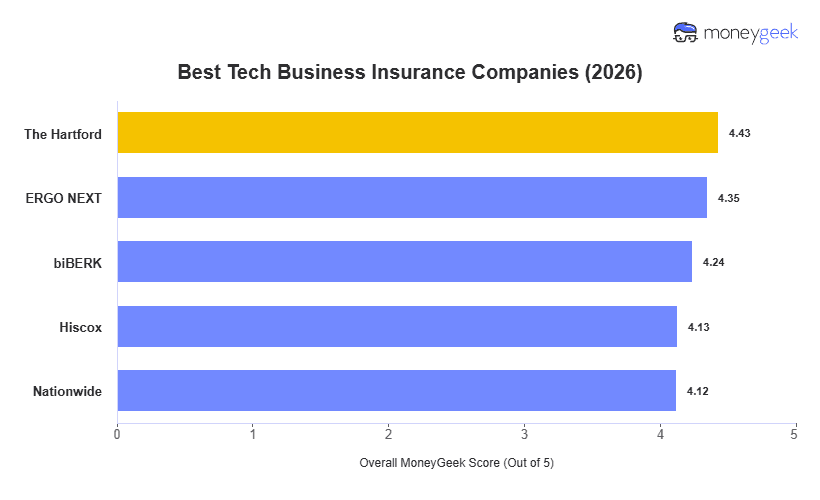

- The Hartford: Best Overall, Best for Tech Startups and Software Firms

- ERGO NEXT: Best for Customer Experience

- biBERK: Best for Direct-to-Carrier Coverage

- Hiscox: Best for Cyber and International Coverage

- Nationwide: Best for Extensive Coverage Options

Each of these providers ranked well because they balance what tech businesses actually need from an insurer: pricing that holds up at renewal, coverage options that account for software liability and data risk, and service that doesn't slow operations down when a claim or policy question comes up. The table below allows you to compare our top options side-by-side in terms of overall scores and our main three rating dimensions of cost, customer experience and coverage.