Commercial insurance costs for contractors and those in construction are expensive, sitting at a rate of $190/mo ($2,274/yr) in aggregate across the six most common coverage types and all 50 states for a 1-to-4-person company. This makes it the 3rd most expensive industry area to operate in, only trumped by manufacturing and wholesale/distribution. This is primarily due to the broad and frequent risk of claims due to the high rates of property damage, tools and equipment theft and injury to both the public and employees associated with the work area.

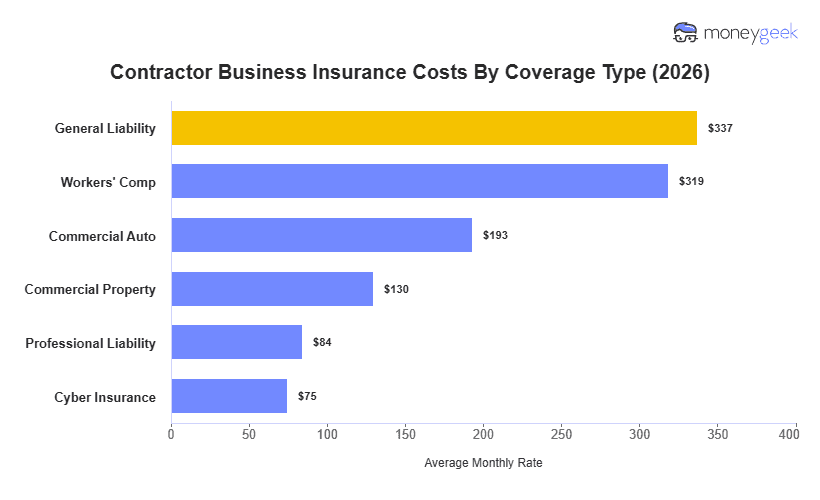

Considering these assumptions, a single policy's on average price can sit anywhere from $75/mo for cyber insurance up to $337/mo for general liability policies. If you are a tradesperson or contracting company, you'll have some of the highest costs, regardless of what policy you choose. Though keep in mind, this doesn't apply to every company, and particularly your industry area and employee count will impact the costs heavily. Your location is more supplementary when compared to these factors, especially for liability focused policies.