Contractor insurance costs for electricians rack closely with the overall average for its general industry category. My analysis of proprietary rate data puts the average at $190 per month, or $2,279 per year, across five common coverage types for businesses with one to four employees across all 50 states and Washington, D.C.

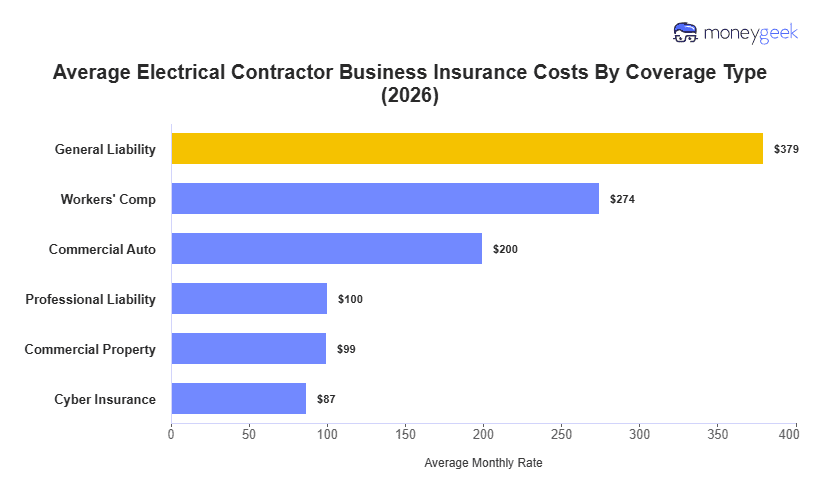

General liability at $379 per month is the highest cost policy figure across all types studied, pricing high due to risks like wiring errors and code violations create fire and safety exposure that can surface years after a job closes. Workers' comp costs at $274 per month per employee reflects live systems, elevated work, and confined space exposure. On the other end, commercial property at $99 stays relatively modest since most small electrical contractors aren't carrying significant owned inventory beyond tools and a van.

The table below reflects benchmark averages for electricians by coverage type, not carrier-issued quotes.