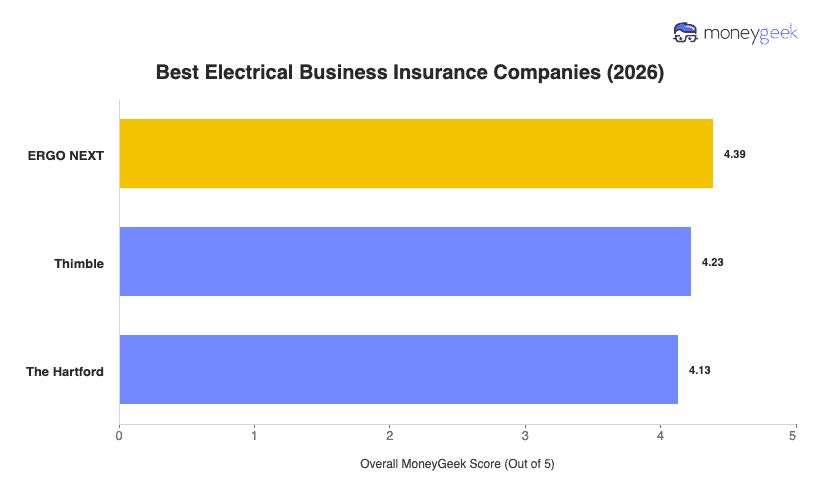

No one carrier is has best insurance for contractors dealing with electrical work. ERGO NEXT tops my analysis overall, but your right fit depends on the jobs you take, the clients you work with, your business size and whether you have employees. If you’re a solo electrician doing residential repairs, an affordable policy with general liability and tools and equipment coverage could be enough. But if you take commercial jobs, panel upgrades or employee-based projects, you'll need higher limits, a more complex coverage mix and a provider with stronger support for certificates, endorsements and claims.

Use the table below to see which provider matches your businesses' needs: