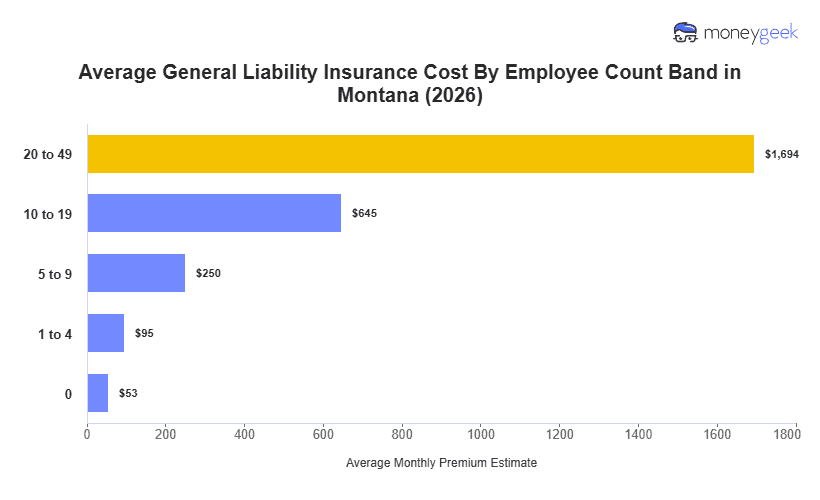

The average cost of general liability insurance in Montana is approximately $95 monthly, or $1,139 annually, for businesses with one to four employees. This sits about 23% below the national average, placing Montana among the five most affordable states for this coverage.

Among Mountain West states, Montana anchors the low end of a $51 monthly spread that runs up to $146 in Colorado. Idaho ($97), North Dakota ($96) and New Mexico ($102) cluster near Montana, while Wyoming ($106) and Utah ($110) sit mid-range. Only Nevada ($131) and Colorado exceed the national average. This pattern likely reflects differences in litigation environment, population density and commercial claim frequency, with Montana's lower claim activity helping explain its position at the affordable end of the region.

If your quote falls near the state average, you're tracking with typical Montana pricing. A quote well above that range raises a question: which factors, such as industry classification, coverage limits or claims history, are driving the difference?