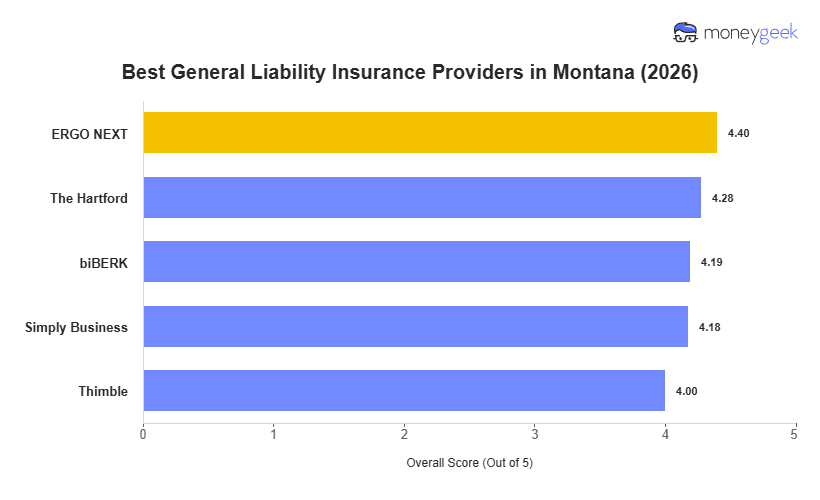

Not every general liability provider fits every Montana business as risks, coverage needs and budgets vary. We evaluated 10 insurers at $1 million per occurrence/$2 million aggregate limits to find the best and cheapest options available. The five providers below rose to the top across a wide range of business types, so start your comparison here.

- ERGO NEXT: Best Overall, Best for Hands-On Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Fitness and Recreation Businesses

- Simply Business: Best for Comparing Carriers

- Thimble: Best for Short-Term and Seasonal Coverage

See each provider's rates and rankings in the table below. A fishing outfitter near the Yellowstone River and a ranch supply store in Great Falls have different liability exposures. Compare costs side by side to find coverage that fits your operation and budget.