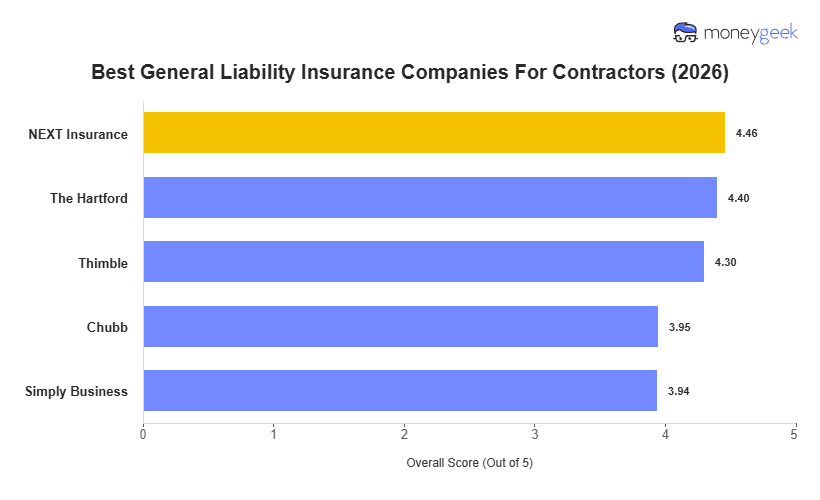

In short, the 3 best general liability insurers for contractors that had the most ideal balance of affordability, service and coverage are the following:

- ERGO NEXT: Best Overall, Best For Lower Risk Contractors

- The Hartford: Best For Value Coverage and Larger Operations

- Thimble: Best For Gig and High-Risk Work

As you can see by their awards, each insurer has specialties in terms of where they are best, and no one insurer is a fit for everyone. So, keep in mind these providers are a good starting point, but the number one pick overall is not necessarily right for you. I've also broken down the rankings of the top 5 that made the cut in the table below for side-by-side performance comparisons.