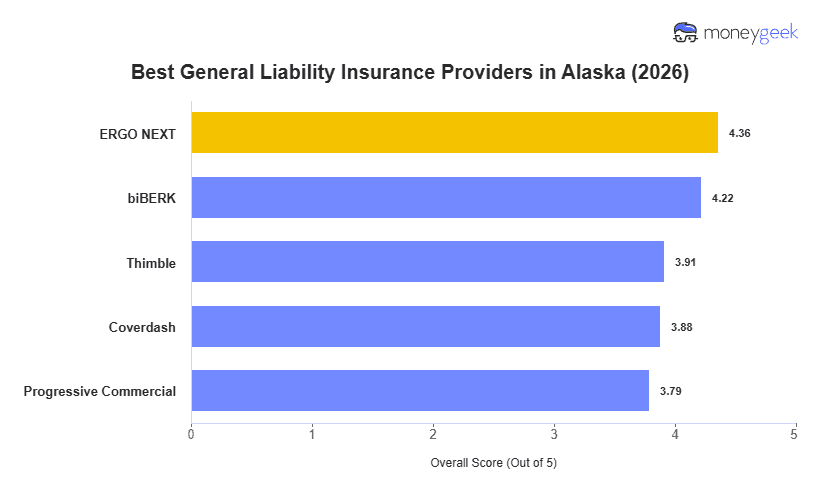

Alaska businesses carry different risks, but these five general liability insurers consistently rank among the most affordable and reliable statewide. We analyzed 10 major providers using standard $1 million per occurrence/$2 million aggregate limits, scoring each on pricing, service quality and coverage strength to identify top performers.

- ERGO NEXT: Best for Hands-On and Customer-Facing Businesses

- biBerk: Best for Service and Wellness Businesses

- Thimble: Best for On-Demand Coverage

- Coverdash: Best for Multiple Carrier Comparisons

- Progressive Commercial: Best for Wholesale and Distribution

These insurers balance affordability with dependable claims service for Alaska businesses managing seasonal operations, remote locations and harsh winter conditions. The table below compares their rates and rankings, whether you run a fishing charter in Juneau, a construction company in Anchorage or a retail shop in Fairbanks.