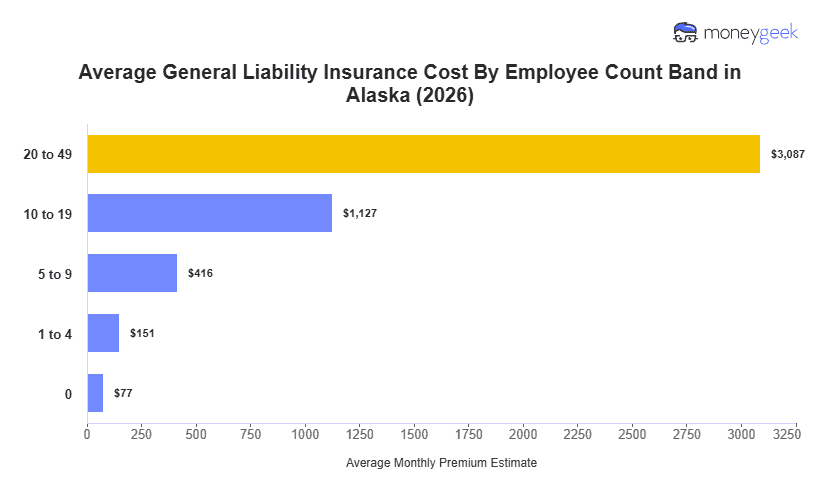

The average cost of general liability insurance in Alaska is $151 per month, or $1,815 per year, for businesses with one to four employees with limits of $1 million per occurrence/$2 million aggregate. That run 23% above the national average of $123 monthly and places Alaska 42nd in affordability.

Every state in the Pacific region exceeds the national benchmark, and Alaska's premium reflects that broader regional pattern. Higher labor costs, elevated construction and property values, and a concentration of litigation-active markets push claim costs up across the region, which flows into base pricing. Oregon is the least expensive in the group at $138 per month, while Washington ($153) and Hawaii ($159) sit just above Alaska. California is a clear outlier at $190 monthly, 55% above the national average.

Use the state average as a regional reference point. Coverage limits, industry risk profile and claims history can move actual premiums in either direction, so treat this figure as orientation, not a projection. To get a cost estimate based on your business profile, use the Alaska general liability insurance cost calculator below.