Our analysis of Alaska professional liability insurers found three providers that consistently outperformed the field on rates, coverage quality and customer experience.

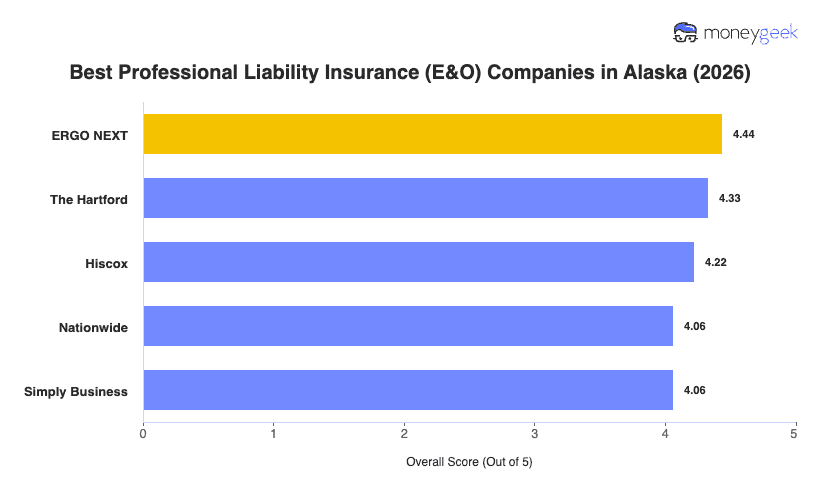

- ERGO NEXT: Ranking first across 11 of 18 industries in Alaska, it earns its top spot through competitive pricing and a fully digital buying experience that gets you from quote to active policy in under 10 minutes. That matters in Alaska, where you can't always walk into an agent's office in Fairbanks or a remote job site community. ERGO NEXT covers over 1,300 business types and gives you 24/7 access to certificates of insurance without having to call anyone. Education businesses find better value elsewhere, and financial services and consulting professionals should compare closely before committing.

- The Hartford: Claims handling strength and a 200-plus year track record set The Hartford apart, particularly for Alaska's real estate professionals, cleaning businesses and beauty and wellness services, where it ranks first statewide. It earns top marks for affordability, and its agent-supported buying process works well for businesses that want to talk through their options rather than click through a form. Health care providers and businesses in the other professional services category will find stronger fits with ERGO NEXT or Hiscox.

- Hiscox: Tech professionals and IT consultants in Alaska get the best match with Hiscox, which ranks first statewide for that industry and covers over 180 business types with policies built around profession-specific risk. Its financial strength ratings are among the best in this group, and its complaint record runs below the industry average. Childcare providers, nonprofits, fitness businesses and pet care services also rank Hiscox in the top two statewide.

These three providers cover the best fit for most Alaska businesses, but no ranking accounts for every variable your operation brings. Comparing business insurance options side by side and pulling quotes directly from each carrier gives you a cleaner picture than any list can.