An IT consultant mid-project and a life coach building a solo practice carry different risks, serve different clients and need different coverage, so no single provider is the best fit for every consulting business. Our analysis of the seven top business insurance companies for consultants found five providers that hold up well whether you're matching E&O limits to a client contract, covering subcontractors or scaling coverage as your practice grows.

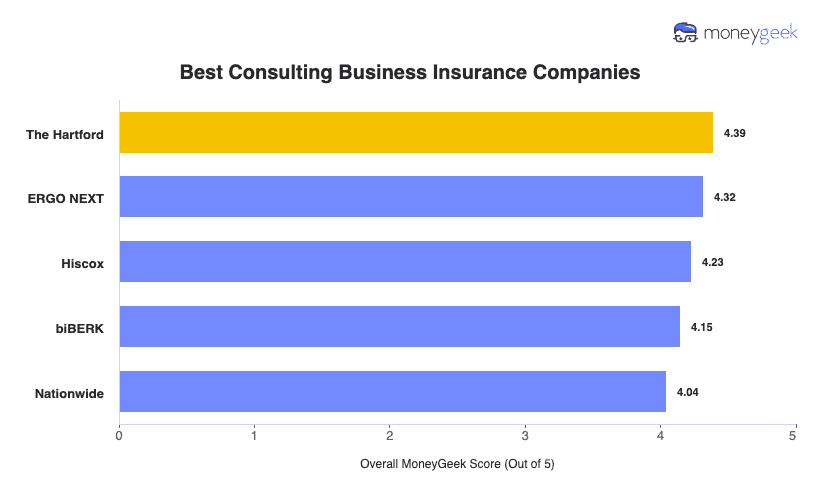

- The Hartford: Best Overall, Best for Growing Consulting Firms

- ERGO NEXT: Best for Customer Experience

- Hiscox: Best for International Consulting Coverage

- biBERK: Best for Straightforward Consulting Needs

- Nationwide: Best for Complex Coverage Needs

Each carrier ranked well because it delivers on pricing consistency, service quality and coverage options built around how consulting work is actually structured. They don't all lead on every area, but whether you're an independent management consultant, a growing IT firm or a specialist brought in on client contracts, you'll find a good option from this group. The table below breaks down how they compare.