While there is no single best business insurer for every cleaning business, some providers are better suited to the industry as a whole. After analyzing affordability, customer experiences and coverage options across major insurers, I found these providers are the top options for cleaners.

Best Cleaning Business Insurance

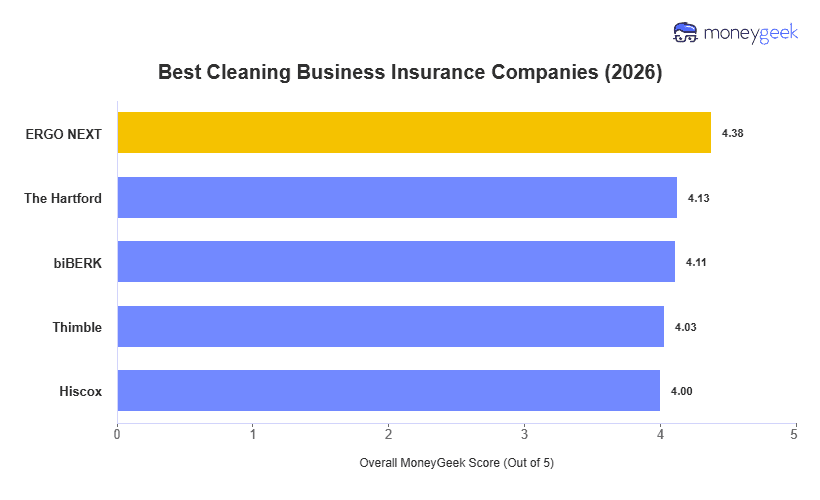

I found that ERGO NEXT, The Hartford and biBERK are the best cleaning business insurance providers offering the most coverage value to small companies. However, your subindustry, location, business size and coverage needs all shape which carrier fits best.

If you want coverage now, MoneyGeek can match you to your best cleaning business insurer with our tool based on your profession and state.

Select state

Updated: June 24, 2026

Advertising & Editorial Disclosure

Key Takeaways

ERGO NEXT is my pick for the best cleaning business insurer overall, earning a score of 4.38 out of 5 for its balance of affordability and customer experience.

Most cleaning businesses should start with general liability, then add tools and equipment, commercial auto and workers’ compensation as their risks and requirements grow.

Depending on your business's growth stage, your best insurer will vary. Prioritize cost and easy-to-use tools when just starting out, but as you grow, value agent support, broad coverage and risk management tools more in your decision.

Best Cleaning Business Insurance Companies

ERGO NEXT | Best For Most Small Cleaning Companies | 4.38 | $72 | Fast online quotes, instant COIs, affordable rates and easy policy tools |

The Hartford | Best For Growing Cleaning Companies | 4.13 | $89 | Broad liability coverage, agent support, risk management resources and strong claims support |

biBerk | Best For Cleaner Liability and Auto Bundles | 4.11 | $90 | Direct coverage, commercial auto availability, simple contracts and Berkshire Hathaway backing |

Thimble | Best For Seasonal or Part-Time Cleaners | 4.03 | $81 | Hourly, daily and monthly coverage options that can reduce costs for occasional jobs |

Hiscox | Best For Specialty Cleaning Services | 4.00 | $86 | 120-year business insurance focus and broad professional liability options |

This list gives you a good starting point, but I would not choose a cleaning business insurer based only on rank. The best provider depends on how your business operates, who you clean for and how much support you need managing coverage.

Below, I break down why each provider made my list, who it serves best and when it may be a less ideal option.

For my overall best cleaning business insurance ratings, I analyzed pricing, coverage options, and customer experience across 16 subindustries and all 50 states and Washington, D.C.

My analysis focuses on 1-to-4 employee businesses, which represent nearly half of the U.S.'s small companies, while weighting results to ensure broader industry and location representation. To do this, I evaluated over six million business profiles, more than 300,000 customer experience data points and performed in-depth analysis of coverage contracts and endorsements to compare insurers consistently across industries and regions.

I then rated each company across affordability (50% of the overall score), customer experience (30% of the overall score), and coverage options (20% of the overall score) to form an overall rating.

See our full methodology.

ERGO NEXT

Best For Most Small Cleaning Companies

ERGO NEXT is my top pick for cleaning business insurance because it ranked first across all 16 cleaning subindustries in my analysis and ranked first on price and customer experience. Its best fit is small cleaning companies with fewer than 10 employees that want affordable coverage, fast online quotes, instant COIs and simple digital policy management.

Its main limitation is coverage depth. ERGO NEXT handles standard cleaning risks well, including general liability, workers’ comp and tools and equipment as an add-on, while commercial auto and cyber coverage are available through partners. However, cleaning companies that need higher limits, uncommon endorsements, stronger claims or agent support are likely better served by a more experienced.

Learn More: ERGO NEXT Business Insurance Review

The Hartford

Best For Growing Cleaning Companies

The Hartford is my top choice for cleaning businesses that need broader coverage and more support than a basic general liability policy provides. Its BOP can bundle general liability, commercial property and business income coverage, and cleaning businesses can also add workers’ comp, EPLI, umbrella, cyber coverage, and more to build a complete policy package.

Though these benefits come at a higher premium, and The Hartford is not the cheapest option in my analysis,its agent-supported buying process may feel slower than a fully digital insurer. But for established cleaning companies with employees, commercial contracts, equipment exposure or higher coverage requirements, that extra support can be more valuable than getting the lowest rate.

Learn More: The Hartford Business Insurance Review

biBerk

Best For Cleaner Liability and Auto Bundles

biBerk is a strong fit for cleaning businesses that want to buy coverage directly from an insurer and keep multiple policies in one place. As part of the Berkshire Hathaway Insurance Group, biBerk brings financial stability that many online-first insurers cannot match, while still offering a simpler direct-buying process than traditional agent-led carriers.

Its biggest advantage for cleaners is coverage breadth. biBerk offers common cleaning business coverages such as general liability, workers’ comp, BOP, commercial auto, professional liability, umbrella and cyber. That makes it a practical option for cleaning companies that need more than basic liability coverage, especially if vehicles or bundled policies are part of the insurance decision. However, claims experience ranked lower in my analysis, and some policy changes may require a phone call rather than a fully online update.

Learn More: biBerk Business Insurance Review

Thimble

Best For Seasonal or Part-Time Cleaners

Thimble is the best fit for cleaning businesses that do not need a traditional annual policy all the time. It is the only provider in my analysis that lets cleaners buy coverage by the job, month or year, which can help solo cleaners, part-time operators and seasonal businesses avoid paying for coverage they do not need.

Its flexibility is most useful for cleaners who move between job sites, take occasional contracts or need proof of insurance quickly for a specific client. Thimble offers common coverage types such as general liability, workers’ comp, BOP, professional liability, business equipment protection and cyber, but it does not offer commercial auto for cleaning businesses that own or lease vehicles. It is also less competitive for larger cleaning companies because affordability drops as employee count increases, and claims support is more limited than with other larger insurers.

Learn More: Thimble Business Insurance Review

Hiscox

Best For Specialty Cleaning Services

Hiscox is a strong fit for cleaning businesses that want a straightforward online buying process but still value access to licensed agents before purchasing. It has focused on business insurance for more than 120 years, carries an AM Best A rating and offers core coverage options for cleaners, including general liability, BOP, professional liability and cyber insurance.

Its best pricing in my analysis showed up for more specialized cleaning work, including air duct cleaning, chimney sweeping and hood cleaning. Hiscox is less competitive for standard residential and high-volume cleaning operations, and it may add friction after purchase because policy changes require agent contact. Commercial auto is also not available through its standard online quote flow, so cleaners with owned vehicles may need another provider.

Learn More: Hiscox Business Insurance Review

Best Types of Cleaning Business Insurance

The best cleaning business insurance policy starts with general liability, but most cleaners eventually need more than one coverage type. I've listed the most commonly needed coverage types for small cleaning companies below, so you can simplify creating your ideal bundle.

All cleaners need this | Third-party bodily injury, property damage and advertising injury claims. | If you damage a client’s floors, furniture or fixtures, this is usually the first policy that responds. It can also help with injury claims tied to your work. | |

Required once you hire employees | Employee medical costs, lost wages and work-related injury or illness claims. | Cleaning crews face slip, lifting, repetitive strain and chemical exposure risks, making this essential once you have employees. | |

Needed if you frequently bring equipment to job sites | Repair or replacement of business equipment damaged, lost or stolen away from your main business location. | Vacuums, carpet cleaners, floor buffers, pressure washers, ladders and supplies may need protection while stored in a vehicle or used off-site. | |

Required if you use vehicles for business | Accidents, injuries and property damage involving business vehicles, depending on the policy. | Regular travel between homes, offices or job sites can create business driving exposure that personal auto insurance may not cover. | |

Only needed if you want to protect equipment kept at a physical location | General liability plus commercial property coverage, and often business income coverage. | A BOP can fit cleaners with an office, storage space or business property that would be expensive to replace after a covered loss. | |

Needed to build trust with clients or as a requirement in commercial contracts | Client losses caused by employee theft or dishonesty, depending on the bond terms. | Clients may ask for bonding before giving cleaners unsupervised access to homes, offices, apartments or commercial spaces. | |

Mainly needed if you offer more specialized services and have stringent contractual requirements | Claims that your service error, advice, negligence or failure to perform caused a client financial loss. | Commercial contracts, specialty cleaning methods or service standards can create disputes that are not limited to bodily injury or property damage. | |

How The Best Cleaning Business Insurance Changes as Your Company Grows

The best cleaning business insurer changes as your company grows because your risks, contracts and day-to-day insurance needs change. A solo residential cleaner balances client work, scheduling, sales, bookkeeping and proof-of-insurance requests alone, so a low-cost insurer with fast online quotes, instant COIs and simple policy management is the best fit.

That changes as your company adds more employees, vehicles, equipment and commercial contracts to the mix. Once you get past the point of a smaller operation below 5 employees, a larger insurer with more dedicated industry-level expertise, risk management support and more specialized coverage options is necessary.

To put this in focus, I've given you a timeline of coverage needs and provider fit from owner-operated up to a larger 20-49 person mid-sized organization.

Solo cleaner: 0 employees | You manage the jobs, client communication and insurance paperwork yourself. Coverage needs are usually simpler, but fast proof of insurance can still affect whether you win work. | ERGO NEXT is the strongest overall fit for affordable coverage, fast COIs and digital tools. Thimble may fit if you only need short-term liability coverage. biBerk should be compared if you need commercial auto directly. |

Small team: 1–9 employees | Employee injuries, supervision, theft concerns and recurring COI requests become more important. You may still want simple servicing, but the insurer needs to support more than a solo operation. | ERGO NEXT remains a strong option for affordable coverage and easy servicing. biBerk is the better fit if you want direct coverage from one insurer and commercial auto is part of the decision. |

Established cleaning business: 10–19 employees | Multiple crews, more equipment, larger jobs and client contract requirements make insurance harder to manage with a basic policy. Support, limits and coverage flexibility start to matter more. | The Hartford is stronger for broader coverage options, agent support and contract needs. biBerk is the better option from my list if direct commercial auto coverage is a priority. |

Larger small business: 20–49 employees | Payroll, claims exposure, vehicles, equipment tracking and client contracts become more complex. The cheapest or fastest policy may not be the best fit if you need help managing coverage changes. | The Hartford is the strongest fit for broader support, claims help and coverage depth. biBerk may fit better if you want a direct buying model and need commercial auto from the same provider. |

Best Cleaning Business Insurance Checklist

Use this checklist process to narrow down the best provider for your cleaning company and the coverage that fits your needs.

- 1Assess Your Cleaning Business Risks

Start by identifying what could go wrong during a normal job. For example, a cleaner could scratch a client’s hardwood floor, spill chemicals on a countertop, slip while carrying equipment or have supplies stolen from a vehicle. If you have employees, they could also get injured lifting machines, climbing stairs or working around cleaning products. These risks help determine which coverage types matter most before you compare insurers.

- 2Match Risks to Coverage Types

Once you know your main risks, connect each one to the policy that would respond to it:

- General liability can help with client property damage or injury claims.

- Workers’ compensation applies when employees get hurt on the job.

- Tools and equipment coverage protects cleaning machines and supplies used away from your main location.

- Commercial auto or another approved business-driving policy may be needed if you or employees drive between job sites.

- A janitorial bond can also help when clients want protection against employee theft.

- 3Set the Right Limits and Requirements

After choosing coverage types, make sure your limits match your cleaning work and client requirements. A solo house cleaner may only need basic liability limits and proof of insurance, while a commercial janitorial company may need higher limits, additional insured endorsements and certificates of insurance for property managers or office clients. If you work with larger contracts, check the insurance requirements before buying so you do not choose a policy that cannot meet them.

- 4Compare Provider Fit

Evaluate providers based on how well they fit your cleaning business, not just which one is cheapest.

- ERGO NEXT fits small cleaners that want affordable coverage, fast COIs and simple digital tools.

- Thimble works better for short-term or job-based coverage.

- biBERK is the best option from our list if commercial auto needs to be handled directly.

- The Hartford is better for broader coverage, higher limits and agent support

- Hiscox fits specialty cleaning businesses or professional liability needs.

- 5Request Quotes and Review Policy Details

Request quotes only after you know your services, coverage types, limits and client requirements. Use the same information for each quote, including your location, payroll, number of employees, services performed, vehicles, equipment and requested limits. Before buying, check what the policy excludes, whether COIs and endorsements are easy to get, how business driving is handled and whether the monthly price changes with annual payment, higher limits or added coverages.

Best Cleaning Business Insurance: Bottom Line

ERGO NEXT, The Hartford and biBerk rank highest overall for cleaning business insurance. The right fit depends on what your operation needs most right now: stable pricing as you scale, fast COI turnaround for commercial contracts or coverage depth for higher-risk work. Rank each carrier against your current situation, not the overall score.

Best Cleaning Business Insurance: Next Steps

To see how costs break down for your specific sub-industry, check the cost and coverage pages for your type of cleaning operation before committing to a carrier.

If you're ready to move forward, focus on getting quotes from two or three carriers that match your sub-industry, coverage mix, and state. Compare them on the same terms, same limits and same structure, so the difference you're evaluating reflects the carrier, not the policy.

If your cleaning business works under commercial contracts

Most commercial clients require a certificate of insurance before work starts, and some specify minimum liability limits in the contract. Review any contract language before choosing your coverage limits.

If you've added higher-risk services like pressure washing or hood cleaning

Check your coverage limits again and make sure your carrier actually writes coverage for that type of work before taking on new commercial accounts.

If you're not sure whether to buy all your policies under one carrier

Managing general liability, commercial auto and workers' comp under one carrier simplifies renewals and policy management, but not every carrier writes all three for cleaning businesses. Confirm coverage availability before committing to consolidation.

If your crews work across more than one state

Carriers handle multi-state operations differently. Confirm that any carrier on your shortlist writes coverage in every state where your crews work, not just where the business is registered.

About Angelique Palenzuela-Cruz

Angelique Palenzuela-Cruz is a Business Insurance Content Writer at MoneyGeek, where she specializes in general liability, workers’ compensation and professional liability insurance. Her work helps small business owners understand how these policies apply to coverage, including risks like customer injuries, employee injuries, professional mistakes, client contract terms and industry-specific coverage requirements.

She primarily covers service-based businesses where liability and employee coverage decisions are especially important, including cleaning, consulting, beauty and wellness, childcare, education, fitness, food service, pet care, repair and maintenance, and other professional services.

Before joining MoneyGeek, Angelique spent nearly 12 years at Guthrie-Jensen Consultants, one of Southeast Asia’s largest management training firms, where she advanced from Training Consultant to Managing Consultant. In that role, she worked with business clients to assess operational needs, develop training programs and present performance analyses to executive decision-makers. She also helped establish Gladwin Training Consultancy, where she served in learning solutions and client service roles.

Her background gives her practical context for writing about how businesses operate, manage client expectations, structure teams and make risk decisions. At MoneyGeek, she applies that experience to business insurance content, connecting coverage to actual business needs.

LinkedIn: linkedin.com/in/ma-angela-cruz

Email Contact: angelique.palenzuela@moneygeek.com