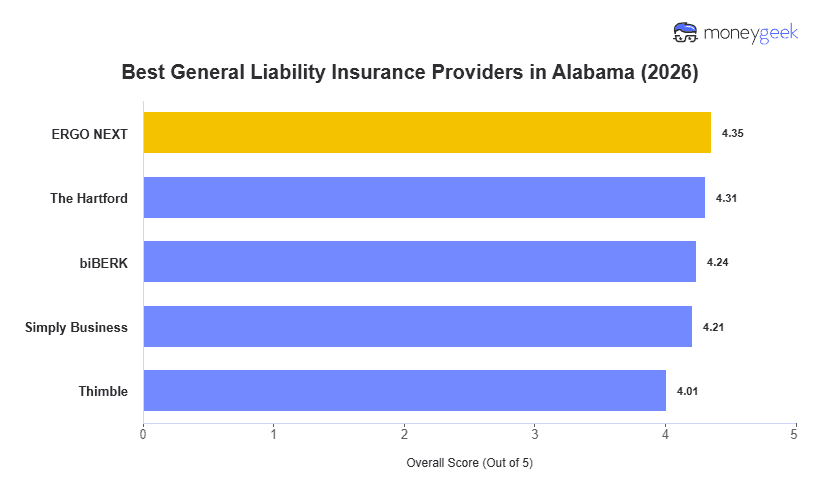

We analyzed 10 major insurers across 25 general industries, using standard $1 million per occurrence/$2 million aggregate limits, to identify the best and cheapest general liability options for Alabama small businesses. No single provider fits every operation, but these five ranked consistently across the measures that matter most:

- ERGO NEXT: Best Overall, Best for Hands-On and Trade Businesses

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Service and Wellness Businesses

- Simply Business: Best for Comparing Carriers

- Thimble: Best for Short-Term and On-Demand Coverage

Whether you run a landscaping crew in Huntsville, a retail shop in Mobile or a contracting business in Birmingham, the right general liability policy comes down to how well a provider holds up when it counts. The table below shows how these five providers rank and what small businesses across Alabama can expect to pay.