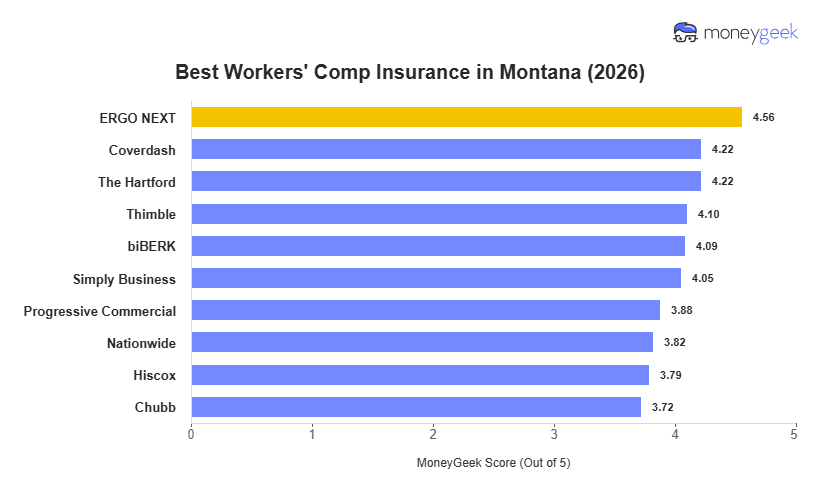

ERGO NEXT offers the best workers' comp insurance in Montana at $62 per month, with top affordability and customer experience scores in MoneyGeek's analysis. Coverdash and The Hartford are strong alternatives for employers who prioritize coverage breadth or agent support over price.

The $60 per month spread between ERGO NEXT at $62 and Chubb at $122 adds up to $720 per year for price-sensitive Montana businesses. That gap narrows for high-hazard industries where class code differences drive more of the pricing difference than base provider rates.