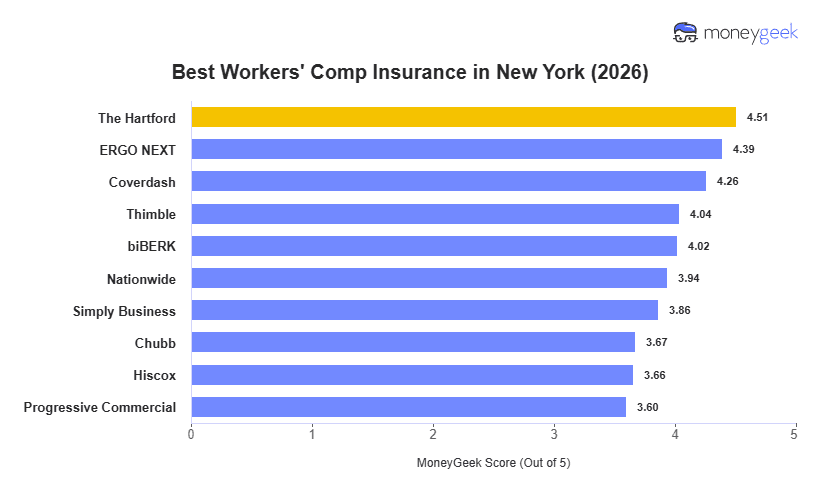

The Hartford is the best workers' compensation insurance in New York, combining the state's lowest rate of $206 per month with broad coverage options and a strong reputation built over 100 years. ERGO NEXT and Coverdash are solid runner-up options, each offering competitive pricing and coverage for New York small businesses.

At $206 per month, The Hartford costs $145 less than Chubb's $351 rate, totaling $1,740 in annual per-employee savings. Employers in lower-risk industries get the most value from that pricing gap. For businesses in high-hazard classifications, the rate difference between providers shrinks because underwriting criteria carry more weight in setting final premiums.