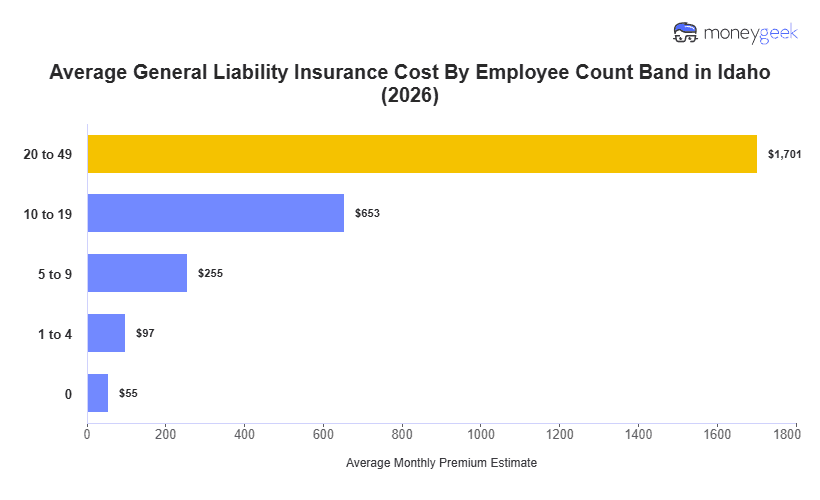

The average cost of general liability insurance in Idaho is $97 per month, or $1,166 annually, for businesses with one to four employees. This benchmark sits 21% below the national average of $123 per month, placing Idaho among the 10 most affordable states for this coverage.

Adjacent states show a clear split: Idaho clusters with Montana at the low end, while Oregon and Washington cost 42% to 57% more. The broader Mountain West region follows a similar pattern: Montana through Utah range from 10% to 23% below the national average, while Nevada and Colorado exceed it by 7% to 19%. Within the mountain region, Idaho ranks second most affordable.

These state averages reflect general patterns, not guaranteed quotes. Final pricing varies based on industry risk, revenue, claims history and coverage limits. When evaluating a quote, Idaho's position offers a useful baseline for comparison. A Idaho general liability insurance cost calculator is available below for a more personalized estimate.