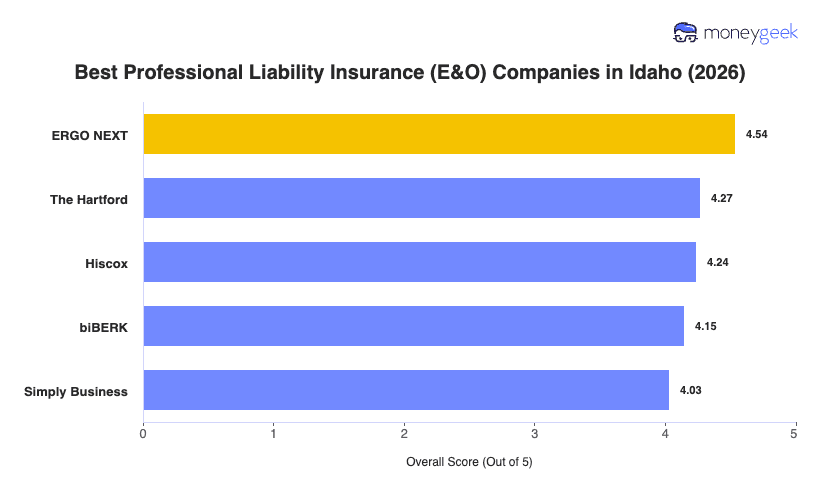

Our analysis of Idaho professional liability insurers identified three providers that outperformed the rest on rates, service quality and coverage.

- ERGO NEXT: Ranked first across nearly every industry in Idaho, with the top affordability score and the highest customer experience score among all reviewed providers. The insurer's digital-first setup makes it easy to get a quote, understand what's covered and bind a policy without back-and-forth. ERGO NEXT suits a wide range of Idaho businesses well, from fitness studios and pet care providers to construction contractors and healthcare practices. The one caveat worth knowing: it ranks sixth in both consulting services and financial services in Idaho, so professionals in those fields should compare options before committing.

- The Hartford: Strong second-place finish driven by its depth in two areas where most competitors fall short. It ranks first in Idaho for both consulting services and financial services, making it the clearest fit for CPAs, financial advisors and independent consultants operating out of Boise or Idaho Falls. The Hartford also has dedicated small business support teams and a long track record handling professional liability claims across a range of industries. It does rank ninth in healthcare and other professional services, so practitioners in those categories should weigh their options.

- Hiscox: Rounds out the top three with solid performance across most industries, particularly in hospitality, tech and real estate. It ranks second for nonprofit organizations and third in consulting, financial services, education and marketing. Policyholders report that Hiscox makes coverage terms easy to understand, which matters for businesses buying professional liability for the first time. Construction and recreation businesses will find better-ranked options elsewhere.

These three providers represent the best fit for most Idaho businesses, but no ranked list covers every situation. Comparing business insurance options side-by-side and getting quotes directly from carriers gives you the clearest picture of what's right for your business.