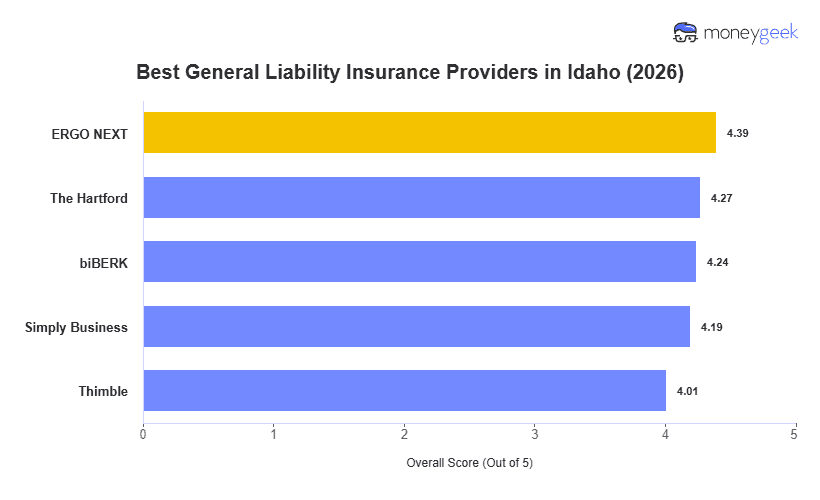

Every business has different coverage needs, so the right insurer isn't always the cheapest one. We evaluated 10 major general liability providers across 25 industries in Idaho to identify the best and most affordable options. These five companies topped our analysis:

- ERGO NEXT: Best Overall, Best for Hands-On Service Businesses

- The Hartford: Best for Health care and Education Businesses

- biBerk: Best for Service-Based Businesses

- Simply Business: Best for Carrier Comparison Shopping

- Thimble: Best for Gig Workers and Freelancers

Whether you run a fly-fishing outfitter near Sun Valley or a potato farm equipment repair shop in Twin Falls, rates and coverage needs will differ. The table breaks down rates and rankings for each provider.